- Can You Use a Bridging Loan to Buy Land?

- What’s the Catch? Is It Easy to Get One?

- How Do Land Bridging Loans Work?

- How to Apply for a Land Bridging Loan?

- Exit Strategies Uncovered

- What Do You Need to Qualify for a Land Bridging Loan?

- Who Offers These Loans?

- What are the Typical Interest Rates?

- How Much Will It Cost You?

- Other Ways To Fund Your Land Purchase

- The Bottom Line

Land Bridging Loans: A Way To Fast Track Your Land Ownership

You’ve found it—the land that perfectly fits your development dreams or investment goals. But there’s a snag: you need quick funds to seal the deal before someone else snaps it up.

What’s your next move? A land bridging loan could be a quick fix you need, but navigating its complexities can feel daunting.

In this guide, you’ll learn everything you need to know about land bridging loans in the UK. From finding the right lender to understanding interest rates, we’ll provide a step-by-step guide to secure your investment successfully.

Can You Use a Bridging Loan to Buy Land?

The short answer is yes.

Much like securing a bridging loan to buy property, you can also take out this type of short-term finance to get your hands on a piece of land.

This is a go-to option for developers eager to lock down an investment, whether it’s a piece of land coming up in an auction or a strategic spot for a future project.

But it’s not just for commercial plots—you can use a land bridging loan for residential land as well.

What’s the Catch? Is It Easy to Get One?

Land bridging loans are unique; they aren’t your run-of-the-mill bank loans. These loans are considered high-risk and usually come from specialist lenders.

It means that you can’t just waltz into any bank and expect to walk out with a loan. But don’t worry, with the right know-how and perhaps a little help from a broker who knows the ins and outs of land bridging finance, you can improve your chances significantly.

How Do Land Bridging Loans Work?

If you need some quick cash, a land bridging loan can get you the funds you need in just a matter of days. However, you should know that this speed comes at a price: higher interest rates compared to more traditional options.

Lenders aren’t handing out free money here; they’ll want to see a solid deposit from you. In some cases, they might even ask you to pledge additional security, like your home.

And since we’re talking about interest-only loans, you’ll also need to show lenders your game plan for paying the loan back. They’ll want to see your “exit strategy“—that might be selling the land later or applying for long-term finance once your land project is a success.

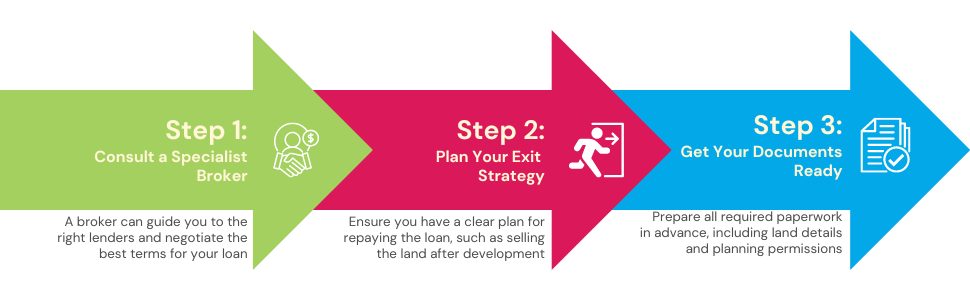

How to Apply for a Land Bridging Loan?

If you’re eager to purchase a piece of land and need to move quickly, a land-bridging loan is one way to make it happen. But what steps should you take to ensure your application is successful? Let’s dive in.

1. Consult a Specialist Broker

First thing first: get advice from an expert. Land bridging loans are not your typical loans, and they can be pricey.

An experienced broker can guide you through the maze, assessing whether this type of loan suits your needs.

Your broker can also steer you toward the right lenders and negotiate better terms for you. Remember, land bridging loans aren’t available to everyone—you’ll generally need a referral from a certified broker to even get in the door.

Want to find the right broker for you? Reach out to us, and we’ll connect you with a qualified specialist in land bridging loans.

2. Plan Your Exit Strategy

Before you go knocking on a lender’s door, have your exit strategy ready to go. These loans can be for large sums—sometimes millions—so lenders want assurance that you can pay it back.

Whether it’s selling the developed land or securing long-term financing, make sure you have a well-thought-out plan. And it wouldn’t hurt to have a Plan B, just in case.

Curious about what makes a good exit strategy? Keep reading; we’ve got the details coming up.

3. Get Your Documents Ready

Time is of the essence with land bridging loans. To keep things moving, gather all the required paperwork beforehand.

Your broker will guide you, but generally, you’ll need comprehensive details about the land, any planning permission or applications in process, and any existing valuation reports.

Exit Strategies Uncovered

Your exit strategy isn’t just a plan; it’s your ticket to loan approval. Here are some popular options:

- Sell the Developed Land – Buy the land, build on it, and then sell it. Use the profits to pay back the loan—it’s as simple as that.

- Sell After Getting Planning Permission – Another option is to secure planning permission first. Once granted, you can sell the land at a higher value and use that money to repay your loan.

- Opt for a Self-Build Mortgage – If you’re building your dream home, a self-build mortgage might suit you. Funds are released in stages as your construction progresses. You can use this money to both fund your build and repay the bridging loan.

- Choose Development Finance – Planning to develop a commercial property? Then a development finance loan is more up your alley. Like self-build mortgages, funds are released in stages, offering another pathway to repay your loan.

- Remortgage Developed Properties – If you’ve developed properties on the land, remortgaging them based on their new value could provide the funds you need to repay the bridging loan.

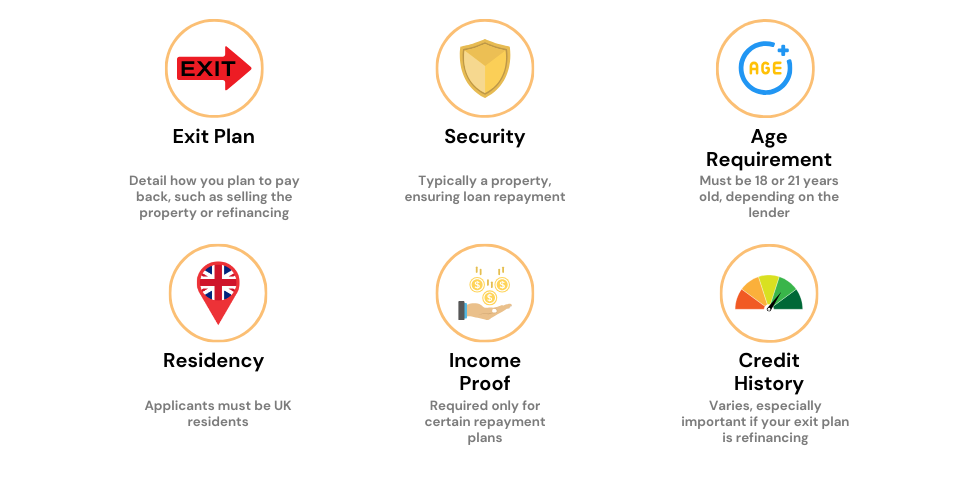

What Do You Need to Qualify for a Land Bridging Loan?

When getting a land bridging loan, there are some boxes you’ll need to tick first. Here’s everything you should know to boost your chances of getting approved.

A Strong Deposit or Valuable Security

To qualify, you usually need a deposit ranging from 35% to 40%. The loan-to-value (LTV) ratio is generally between 60% and 65%.

A bigger deposit could score you a better interest rate. If you haven’t secured planning permission yet, expect to put down about 50%. Cash isn’t your only option; you can also use assets like a home you own as collateral.

A Bulletproof Exit Strategy

Your lender wants assurance that you can pay back the loan. A well-thought-out exit strategy will not only boost your appeal but also could get you a better deal.

Always have a backup plan ready. And don’t forget, you’ll need to repay the full loan amount at the end since these are interest-only loans.

Clean Credit Score

While a few marks on your credit history won’t automatically disqualify you, a clean credit score will definitely work in your favour. You’re more likely to get approved, and you might even get a more competitive rate.

Experience in the Industry

While it’s not a must-have, having a background in property or land development will give you an edge. Lenders will see you as less of a risk, which could lead to better rates for you.

Planning Permission

You’ll generally need planning permission for the land before getting the loan. A few lenders might still consider you without it, but be prepared to put down a big deposit—around 50%—and possibly offer extra collateral.

Who Offers These Loans?

You won’t find these loans just anywhere; you’ll need a specialised lender. A broker with experience in land bridging loans can help you navigate this specialised field and recommend the best lender for you.

Some Lenders to Consider:

- MFS

- Shawbrook Bank

- MT Finance

- Oakbridge

- KIS Bridging Loans

What are the Typical Interest Rates?

The monthly rate for a land bridging loan is subject to change based on several factors. If you’re eyeing prime real estate and have a solid plan to pay back the loan, you’re looking at interest rates of around 0.9% per month.

However, if you lack planning permission or the land is in a less desirable location, the rate can increase to between 1.25% and 1.5%.

How Much Will It Cost You?

The amount you can borrow isn’t set in stone. It could be as low as £5,000 or go all the way up to a staggering £25 million.

Two things influence this: how much your property is worth and your financial health.

Lenders will usually loan up to 75% of your property’s value. In special cases, especially if this loan is your primary loan against the property, you could qualify for even more.

To get an idea about how much the loan will set you back each month and in total, use our handy calculator below.

[Embedded Bridging Loan Calculator]

Other Ways To Fund Your Land Purchase

If a land bridging loan doesn’t fit your needs, don’t worry. There are other options.

Commercial Mortgage

With a commercial mortgage, you’re looking at a longer-term loan with the land as your collateral. The minimum loan term is usually 15 years. However, rates are generally higher than residential mortgages due to the higher risk involved.

Development Finance

Development finance is similar to a bridging loan, but funds are released in stages to support the construction of a new property or the renovation of an existing one. Like bridging loans, development loans require a solid exit plan and have higher interest rates than regular mortgages.

Remortgaging Existing Property

Another way to get the cash is by remortgaging properties you already own. But beware—this is risky. If you can’t keep up with the payments, you could lose your existing properties.

The Bottom Line

Deciding on a land bridging loan is a big step. It’s known for its speed and flexibility, but you need to think it through carefully.

First, ask yourself if it’s the best way to finance your land purchase. Maybe a regular mortgage would be better.

It’s important to have a clear plan for how you’ll repay the loan and to know all the costs involved, including interest rates and extra fees.

If all of this feels a bit overwhelming, don’t worry, you’re not alone. This is where an expert can be a huge help.

Specialised land-bridging finance brokers can provide personalised advice. They’ll explain everything in simple terms and guide you through your loan options. And if you’re considering other types of loans for your land purchase, make sure your broker knows about those too.

Expertise in this area is rare, but we can connect you with the right specialist. Just fill out this form, and we’ll introduce you to a broker who can streamline the process and find you the best deal.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I use bridging finance for land?

Yes, you can use bridging finance to buy land. It’s a short-term loan option for land acquisition.

Does the land need planning permission?

It depends on the land’s current status. Some land already has planning permission, while others don’t. You can still get bridging finance for land without planning permission if you have a plan to obtain it.

Who uses land-bridging finance?

Different people and businesses use it:

- Property developers – They use it to buy land quickly for construction while securing long-term financing.

- Investors – It’s handy for buying land or property for investment, like rental properties or commercial real estate.

- Homebuyers – It helps when you’re buying land for a new home and need to bridge the gap between selling your current property and buying the land.

- Companies & Businesses – Useful for diversification, expansion, development, or speculation.

- Auction buyers – It’s common at property auctions where quick payment is often required.

What do I need for a land loan application?

When applying for a land bridging loan, lenders typically need:

- Details about the land or property you’re buying, including location, size, and any planning permissions.

- Personal or company financial information, such as income, assets, and liabilities.

- A clear plan for repaying the loan, like through land or property sale or remortgaging.

- Relevant documents like valuation reports, identification, and legal paperwork.

What's the difference between land with and without planning permission?

Land with planning permission already has approval for specific uses, making it more valuable and appealing to lenders and developers.

Land without planning permission doesn’t have pre-approved development rights but can still be eligible for bridging finance if you have a plan to get those permissions.

What is "Hope Value" in land speculation?

“Hope Value” is the potential increase in land value because you expect to get planning permission in the future. It’s the added value based on this expectation. People sometimes buy land hoping to secure planning permission but keep in mind it’s not guaranteed, and local planning policies can affect the outcome.

Related Articles

An In-Depth Guide To Secured and Unsecured Bridging Loans

If you’re in the UK and planning a big move—maybe you’ve found your dream home or you’re eyeing a property investment—you’ve got some financial decisions to make. One of them is choosing between a secured and an unsecured loan. Why does this choice matter? The loan you choose impacts your interest rate, borrowing limit, required […]

Second and Third Charge Bridging Finance Explained

When cash flow gets tight and traditional loans aren’t cutting it, you don’t have to hit the panic button. Second or third charge bridging loans can be your financial lifeline. Now, you might be thinking, “That sounds great, but what’s the catch?” Well, there are a few nuances you should be aware of, like varying […]

Fast Bridging Loans: How to Apply and What You Need?

Imagine you’ve spotted the perfect property investment—fantastic location, huge potential, and it’s a steal. There’s just one hitch: your assets are tied up, and the clock is TICKING. You’ve been down this road before—missing out because the cash wasn’t there when you needed it. But what if there was a way to make your assets […]