- Can You Get Equity Release Even with Bad Credit?

- Which Credit Issues Are Likely to Be Accepted by Lenders?

- Can You Get Equity Release If You Have Debts?

- Can You Get Equity Release If You Have a County Court Judgement (CCJ)?

- What If You’ve Been Declared Bankrupt?

- Tips to Secure Equity Release with a Poor Credit Score

- Can You Remortgage to Release Equity If You Have Bad Credit?

- Other Options to Consider

- Does Equity Release Affect Your Credit Score?

- Key Takeaways

- The Bottom Line

How To Get Equity Release with Bad Credit?

Imagine this: you’ve worked hard to own your home, and now you’re dreaming of a bit more freedom.

Maybe you want to travel the world, try a hobby you’ve always loved, or just have enough money to enjoy life without worrying so much.

But there’s one thing stopping you—your credit score.

Bad credit might make you think you’re out of options, but that’s not the case.

Equity release is still possible, even if your credit isn’t perfect. Lenders know life can be messy, and they’re often willing to work with you to make it happen.

In this article, we’ll explain how equity release works, how your credit score fits in, and why it’s not such a big problem. We’ll show you how to use your home’s value to improve your finances and reach your goals.

Can You Get Equity Release Even with Bad Credit?

Yes, it’s possible to get equity release even if you have bad credit, but it depends on your situation.

Equity release doesn’t usually involve monthly repayments, so lenders focus less on your ability to pay and more on your home’s value.

The loan is repaid when your house is sold, either after you pass away or move into long-term care, so your credit score isn’t always a major factor.

But, things like other debts or past bankruptcies could still affect your chances.

Speaking to an equity release broker may help you understand your options and find a plan that works for you.

Which Credit Issues Are Likely to Be Accepted by Lenders?

If you’re wrestling with a poor credit score due to minor issues– such as a few missed payments – you’re likely still in the running for equity release.

But, the acceptance of your application largely depends on individual lender terms and conditions.

Some may ask for an excellent credit history, while others are more flexible, accepting more adverse forms of credit. That said, you’re not necessarily locked out even if you have bad credit history.

Can You Get Equity Release If You Have Debts?

Yes, you may still apply for equity release even if you have debts, but the type of debt matters.

If your debts are unsecured, like credit cards, overdrafts, car loans, or personal loans, and you’re keeping up with payments, they usually won’t stop your application.

But, if you’ve fallen behind on payments, some lenders might ask you to use some of the money from equity release to pay off those debts first.

Debts secured on your home, like a mortgage or a loan linked to your property, can make things trickier.

For equity release to work, your new lifetime mortgage has to be the only debt tied to your home. This means if you still owe money on your current mortgage or a secured loan, you might not qualify.

That said, some lenders might let you use the money from equity release to pay off those secured debts. It all depends on the lender and your situation.

Knowing how different types of debt can affect your chances of equity release can help you make the right choice for your finances.

Can You Get Equity Release If You Have a County Court Judgement (CCJ)?

Having a CCJ can make getting equity release trickier, but it’s not impossible.

A CCJ is a legal order that says you owe someone money.

If it’s linked to your property, lenders might see it as a risk because the person you owe could take further legal steps, like forcing the sale of your home to get their money back.

Because of this, most lenders will ask you to pay off the CCJ before they’ll approve equity release.

In some cases, you might be able to use the money from equity release to pay off the CCJ. But this usually means involving a solicitor and depends on the lender’s rules.

If you have a CCJ, it’s worth speaking to an expert to see what options might work for you.

What If You’ve Been Declared Bankrupt?

If you’ve been declared bankrupt, it can make it harder to get equity release. Lenders won’t consider your application until you’ve been discharged from bankruptcy.

Being discharged means you’re officially free from the debts linked to your bankruptcy.

Even though it stays on your record, it shouldn’t stop you from applying for equity release once you’re discharged.

But, it’s important to let your broker and lender know about any past bankruptcies, no matter how long ago they happened.

Being honest about your financial history will help them find the best option for you.

Tips to Secure Equity Release with a Poor Credit Score

Even with a shaky credit score, there are still ways to improve your chances of securing an equity release. Here are some useful tips:

- Get Your Credit Report. Access your credit report from credit reference agencies such as Experian, Equifax, and TransUnion. Check it thoroughly for any errors, and correct any inaccuracies. This can help to boost your score and give a more accurate reflection of your financial health.

- Pay Bills on Time. Paying bills on time is one of the simplest ways to build up a positive credit history. It shows lenders that you’re reliable and less of a risk.

- Reduce Debt. Pay off as much outstanding debt as you can before applying for an equity release scheme. This will also reduce your outgoings, making it easier to meet any future repayments.

- Seek Expert Advice. Consult with a specialist adviser who deals with bad credit equity release. They can provide valuable advice tailored to your situation and help you to find the most suitable lenders.

Can You Remortgage to Release Equity If You Have Bad Credit?

Remortgaging means switching your current mortgage to a new one, either with your existing lender or a different one, often to get better terms or access extra money tied up in your home (this is the equity).

If you have bad credit, remortgaging to release equity can be harder, as traditional lenders tend to have stricter checks compared to equity release providers.

Some lenders might reject your application because of your credit history. However, not all lenders are the same—some are more flexible when it comes to credit issues.

The key is to explore your options. A specialist mortgage broker can help you find lenders who are more likely to approve your application, even with a poor credit score.

If you work on improving your credit and look into the right lenders, you can increase your chances of remortgaging to release equity, even if your credit history isn’t perfect.

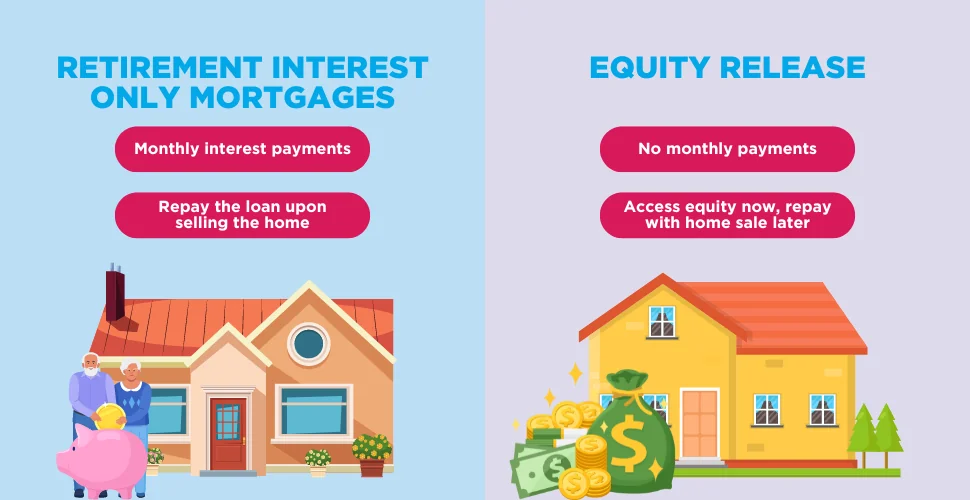

Other Options to Consider

If you’re finding it tricky to get an equity release with bad credit, you might want to consider some alternatives. One of these is a retirement interest-only mortgage (RIO).

RIO is a type of mortgage for people in retirement. With this scheme, you only pay the interest on your loan each month.

Then, when you sell your home, move into long-term care, or pass away, the original loan is repaid.

Here are a few things to know about RIOs:

- Eligibility – You must prove you have enough income to cover the monthly interest payments, usually from your pension.

- Property Sale – Similar to equity release, a RIO also implies that your property will be sold when the loan term ends or in any of the aforementioned circumstances, to repay the original loan.

- No Negative Equity Guarantee – RIOs typically do not offer a ‘no negative equity guarantee’. This means if your property’s sale doesn’t cover the loan, your estate may have to make up the shortfall.

So, while RIOs can be a good option for some, it’s crucial to understand the terms and seek professional advice before choosing this path.

Does Equity Release Affect Your Credit Score?

When it comes to your credit score, getting an equity release won’t usually have a negative impact. If you use some of the funds to pay off other debts, it could even improve your credit situation.

But remember, providers will run a credit check as part of the equity release process. These checks will be recorded on your credit file. Multiple checks in a short space of time can cause a slight dip in your credit score.

That being said, it’s usually only a temporary drop and will recover over time, especially if you’re keeping up with repayments on any debts you have.

It’s always wise to be aware of this when applying for equity release or any other form of borrowing.

Key Takeaways

- You can still get equity release even if you have bad credit, but lenders will look at your home’s value and your overall finances to decide.

- Small credit problems like missed payments might not stop you, but bigger issues like secured debts or CCJs could mean you’ll need to pay those off first, sometimes with money from the equity release.

- If you’ve been bankrupt before, you’ll need to be officially free of bankruptcy (discharged) before applying. You also need to tell the lender about it.

- Remortgaging to get equity can be harder with bad credit, but some lenders are more flexible. A mortgage broker can help find lenders who might say yes.

- If equity release isn’t an option, you could look at other choices like retirement interest-only mortgages (RIOs) or work on improving your credit score to make it easier later.

The Bottom Line

It’s easy to feel stuck when you have bad credit, especially when you know your home could help you sort out your money or achieve important goals.

The whole thing can be confusing, and getting the right advice can be difficult.

That’s why having a specialist to help you makes such a difference.

An expert who understands equity release and bad credit can help you look at your choices, connect you with lenders who offer flexible options, and make the whole process less stressful.

With their help, you can get closer to using the value in your home, even if your finances haven’t been perfect.

Ready to start? Just answer a few quick questions here, and we’ll find you a trusted advisor who’s ready to help.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Will equity release impact my pension credit?

Equity release itself should not directly impact your pension credit. However, if you use the released funds to increase your savings beyond a certain limit, it could affect your eligibility for pension credit.

Always consult a financial advisor before making such decisions.

Is there a maximum age to secure equity release?

Most providers require applicants to be at least 55 years old. There isn’t usually a maximum age limit, but terms can vary between providers.

How quickly can I get the equity from my property?

The timeframe can vary depending on the provider and your circumstances. However, generally, it takes between 10 to 12 weeks from the application to release the funds.

Can I get an equity release if I still have a mortgage?

Yes, it’s possible to get an equity release even if you still have a mortgage. But, you will need to use some of the funds released to pay off your existing mortgage first.

These are just a few of the questions people often ask when considering equity release. Remember, it’s always best to consult with a specialist advisor to get answers tailored to your specific situation.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Can I Sell My House If I Have An Equity Release?

Selling your home with an existing equity release plan requires careful planning. Many homeowners considering a move – be it closer to family, downsizing, or a lifestyle change – often wonder if equity release complicates the sale. The good news is you can absolutely sell! 🎉 However, for a smooth process aligned with your financial […]

Equity Release Companies to Avoid in 2025: 8 Warning Signs

Equity release is a way for older people to get money from their home without having to sell it. It’s a big choice, so it’s normal to feel a bit unsure about which company to trust. Some companies are great, but others might not have the best intentions. So how do you figure out who’s […]

Equity Release Calculator – No Personal Details Required

Lifetime Mortgages are rapidly gaining traction across the UK, becoming a popular option for homeowners in their retirement years. If you’re curious about unlocking the equity in your home, you’ve come to the right place. How Much Equity Can You Release? Our equity release calculator will provide you with an immediate understanding of the equity […]