- What Defines a Large Mortgage?

- Who Needs a Large Mortgage Loan?

- How Much Can You Borrow?

- How Do I Get Approved for Large Mortgages?

- What Is the Minimum Deposit for a Large Mortgage?

- What Are My Repayment Options for a Large Mortgage?

- How to Get the Best Rates on Large Mortgages?

- How Can I Borrow More with a Large Mortgage Loan?

- Who Offers Large Mortgages in the UK?

- How Can Limited Company Directors Secure a Large Mortgage?

- The Bottom Line

What Are Large Mortgage Loans? A Comprehensive Guide

Thinking about buying that spacious family home or investing in a major property?

You might be considering a large mortgage loan. These aren’t just your usual home loans; they’re for when you need more money than the average house purchase.

Large loans help you buy high-value properties or invest big in the housing market.

In this article, you’ll learn about what makes a mortgage ‘large’ in the UK. We’ll also talk about how much you can typically borrow with these kinds of loans. It’s all about giving you the knowledge to make confident choices in the mortgage world.

What Defines a Large Mortgage?

Generally, it’s any loan over £500,000. But this isn’t a strict rule.

Depending on where you are and who you’re borrowing from, what counts as ‘large’ can vary.

For example, in areas with higher property prices, like London, the threshold for what constitutes a large mortgage might be higher.

Lenders pay special attention to large loans. They’re bigger risks, so you might find they ask for more checks on your finances or a bigger deposit than smaller mortgages. And it’s not just about the amount.

Sometimes, a mortgage is called ‘large‘ because it’s more complicated. This could be due to how much you earn, your job type, or the kind of property you’re buying.

It’s important to consult with potential lenders or mortgage advisors to understand how they define and handle large mortgages in your specific context.

Who Needs a Large Mortgage Loan?

Large mortgage loans are designed to help people like you achieve your financial goals and aspirations.

Whether you’re looking to:

- Purchase a luxury home in a prime location

- Accommodate your growing family with a larger home

- Invest in property to generate rental income

- Downsize from a larger property to a more manageable size

- Consolidate your debts into a single, manageable mortgage payment

A large mortgage loan can provide the financial flexibility you need to make your dreams a reality.

How Much Can You Borrow?

The answer varies, but generally, lenders consider how much you earn and your ability to repay the loan. They usually offer loans up to four or five times your annual income.

But, for larger loans, this can sometimes be more, but it comes with stricter checks on your financial situation.

Several factors influence how much you can borrow. Your income is a big one, but lenders also look at your existing debts, your credit history, and your regular outgoings.

They want to make sure you can comfortably manage the loan repayments alongside your other financial responsibilities.

The value of the property you’re buying also plays a role. Lenders need to ensure the loan amount is appropriate for the property’s worth.

It’s not just about the numbers, though. Lenders also assess your job stability and the likelihood of your income remaining consistent or increasing.

If you’re self-employed or have a more complex income structure, you may need to provide additional proof of your financial stability.

How Do I Get Approved for Large Mortgages?

Getting approved for a large mortgage is mainly about proving to lenders that you’re a safe bet. They want to be sure you can handle the repayments.

To increase your chances, take these proactive steps:

- Maintain a Steady Income. Demonstrate consistent earnings through your employment history and pay slips to strengthen your application.

- Manage Existing Debts. Reduce or eliminate existing debts to enhance your debt-to-income ratio, making you a more attractive borrower.

- Establish a Positive Credit History. Maintain a good credit score by making timely payments and keeping credit utilisation low, significantly improving your approval prospects.

- Select the Right Lender. Research and compare mortgage products from various lenders to find one that aligns with your financial situation and goals.

- Seek Professional Guidance. Consider consulting a mortgage broker who can guide you through the application process, assist in identifying suitable lenders, and negotiate favourable terms.

In terms of documentation, be prepared to provide the following:

- Proof of identity and address

- Proof of income (such as payslips or accounts if you’re self-employed)

- Bank statements

- Any information about your current debts.

- Details about the property and your deposit

What Is the Minimum Deposit for a Large Mortgage?

The minimum deposit for a large mortgage can vary, but it’s typically between 10% to 15% of the property’s value.

However, for really high-value properties or unique borrowing situations, this could be higher.

- Larger Deposits, Better Rates. Generally, the more you can put down as a deposit, the lower your interest rate. Lenders see a larger deposit as reducing their risk.

- Deposit Size and Loan Terms. A bigger deposit not only potentially lowers your interest rate but also affects the terms of your loan. You might gain access to more flexible terms or additional features.

- Lower Loan-to-Value Ratio. Putting in a hefty deposit means you’re borrowing less compared to the property’s worth (a lower loan-to-value ratio), which lenders generally like.

It’s worth noting that while a larger deposit can be beneficial, it’s important to balance this against your other financial commitments and savings goals.

Stretching too far to raise a bigger deposit might not be the best move if it leaves you financially vulnerable in other areas.

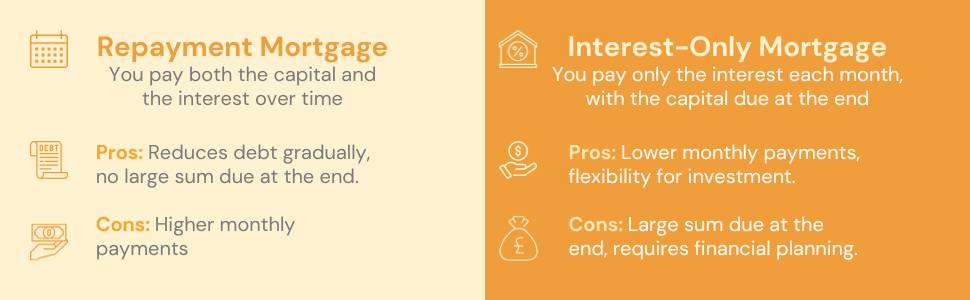

What Are My Repayment Options for a Large Mortgage?

Generally, you have two main options: repayment mortgages and interest-only mortgages.

A repayment mortgage is where you pay back a part of the loan (the capital) along with the interest each month. This means that by the end of your mortgage term, you’ll have paid off the whole loan.

It’s a straightforward approach, giving you the peace of mind that you’re gradually reducing your debt.

Interest-only mortgages involve paying just the interest on the loan each month. The actual loan amount doesn’t decrease over time.

At the end of the mortgage term, you’ll need to repay the original loan amount in full. People often use savings, investments, or the sale of property to pay off the loan.

This option can mean lower monthly payments, but it requires careful financial planning to ensure you can pay off the lump sum at the end.

Which option is best for you depends on your financial situation and long-term plans. Think about how changes in interest rates might affect you and whether you can comfortably manage the repayments alongside your other financial commitments.

If you’re unsure, it’s always a good idea to seek advice from a mortgage advisor. To get more answers, reach out to us.

We’ll connect you to the right advisor who can help you understand the options and decide which repayment strategy best suits your circumstances.

How to Get the Best Rates on Large Mortgages?

Securing a good interest rate is crucial when you’re looking at a large mortgage loan, as even a small difference in the rate can significantly impact the total amount you’ll repay.

Interest rates on large loans are influenced by several factors, including the Bank of England’s base rate, the lender’s costs and policies, and broader economic conditions.

To find competitive rates, start by shopping around. Don’t just check with your current bank; look at what other lenders offer too.

Mortgage comparison websites can be a great tool for this. They allow you to see different rates and terms side-by-side, helping you make an informed decision.

The following factors can also help you secure a good interest rate:

- A good credit history

- A strong financial position

- A large down payment

Lenders may be willing to offer you a lower interest rate as you’re seen as an attractive borrower.

Remember, the best interest rate for someone else might not be the best one for you. It’s always advisable to seek independent financial advice to make an informed decision.

A mortgage broker can help you assess the entire package, including fees, loan terms, and flexibility, and ultimately find the deal that best suits your needs and circumstances.

How Can I Borrow More with a Large Mortgage Loan?

To increase how much you can borrow for a large mortgage, consider these approaches:

- Eliminate Existing Debts. Pay off your current debts to improve your financial standing. Lenders favour applicants with fewer financial commitments. This not only strengthens your appeal to lenders but also bolsters your credit rating, a critical factor in loan assessments.

- Boost Your Income. Elevate your income by negotiating a salary increase or pursuing side jobs. Your borrowing power is closely linked to your earnings. Increasing your income raises the maximum loan amount lenders are willing to offer you for a mortgage.

- Reduce Personal Expenditures. Analyse your spending habits and identify areas where you can cut back. By minimising unnecessary expenses, you free up more funds for mortgage repayments, making you a more attractive candidate for a larger loan.

- Consider Joint Applications. Explore the option of a Joint Borrower Sole Proprietor Mortgage, particularly if you have a lower income. This involves enlisting the support of a family member or friend in your application, potentially increasing the loan amount you can secure. However, this approach entails shared financial responsibility for the loan.

Who Offers Large Mortgages in the UK?

In the UK, a variety of lenders offer large mortgages, each with its offerings:

- Accord Mortgages – Providing loans up to £2 million.

- Aldermore – Offers up to £1 million loans at an 85% loan-to-value ratio.

- Barclays – Known for mortgages as high as £5 million.

- Dudley Building Society – Lends up to £1 million at a 95% LTV and higher amounts at lower LTV ratios.

- Halifax – Another lender with offerings up to £5 million.

- Kensington Mortgages – Specialises in loans up to £2 million at an 80% LTV.

- Nationwide Building Society – Features a cap of £5 million on their lending.

- Santander – Provides loans up to £3 million at a 75% LTV, with flexibility under certain conditions.

Note that these lenders might have a change of criteria and terms. Hence, it’s important to consult with a mortgage advisor to have more options and a better understanding of the current mortgage market.

How Can Limited Company Directors Secure a Large Mortgage?

For limited company directors, securing a large mortgage can be a bit different. Lenders often take a closer look at both your personal and company finances.

You’ll likely need to provide:

- Company Accounts. Detailed records of your company’s financial performance, usually for the last two or three years.

- Salary and Dividend Information. Proof of your income from the company, including both salary and dividends.

- Personal Financial History. This includes your credit score and any other personal financial commitments.

It’s essential to demonstrate the stability and profitability of your company, as well as your financial responsibility.

Some lenders may also consider retained profits within your company when assessing your income.

The Bottom Line

Securing a large mortgage in the UK, while similar to obtaining a standard mortgage, involves dealing with larger sums.

You must understand how factors like your income, credit history, and the property’s value influence your borrowing ability and loan conditions. For company directors, showcasing both business and personal financial stability is key.

While the process is similar to obtaining a standard mortgage, the increased amount adds complexity.

Therefore, consulting with a mortgage broker can be beneficial. They’ll guide you towards a mortgage that aligns with your financial situation and objectives.

Considering a large mortgage? Get in touch with us, and we’ll connect you with a specialist mortgage advisor who can offer tailored advice, helping you navigate through your options to find the most suitable mortgage for your needs.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a large mortgage for a property development project?

No, you generally cannot secure a standard large mortgage for a property development project.

Property development typically requires specialised financing known as property development finance, which is different from standard residential mortgages.

This type of finance is specifically designed to fund large-scale construction or renovation projects and has different criteria, terms, and conditions than a typical mortgage.

For property development, lenders focus more on the project’s potential value and feasibility rather than the traditional factors considered in standard mortgage applications.

What makes obtaining a large mortgage loan challenging?

Large loans are often seen as higher risk than regular ones. Hence, lenders conduct more thorough assessments of your financial health and the property’s value.

Why do high-net-worth individuals face difficulties in securing mortgages?

High-net-worth individuals might struggle to get mortgages because their finances are usually more complex. They often have assets that aren’t quickly sold and incomes coming from different places. This makes it harder for regular lenders to assess their risk, leading to more challenges in getting standard mortgages.

What is the typical processing time for large home loans in the UK?

It usually takes longer than standard mortgages, primarily due to the detailed evaluations and the larger sums involved.

Is it possible to obtain a large buy-to-let mortgage?

Yes, these mortgages are available, but they typically have specific criteria concerning expected rental income and your experience in managing rental properties.

Related Articles

Private Mortgage Lenders Explained

You didn’t get where you are by settling for ordinary, so why start now? Regular mortgages might work for most people, but when you’re dealing with serious wealth, they just don’t measure up. Private mortgages, on the other hand, are in a league of their own. Whether it’s a stunning countryside estate, a sleek London […]

Securing High Net Worth Mortgage In The UK

If you’re wealthy, regular mortgages probably don’t work for you. You need something designed to match your lifestyle and financial goals. The good news? With the right mortgage advisor, buying a high-value property or using your assets for smart investments can be simple. This guide breaks down high-net-worth mortgages in 2025, so you can see […]

The Complete Guide To Asset Based Mortgages In the UK

Lenders often seem to miss the bigger picture when it comes to wealth. You could have millions in property, shares, or investments, but if your income doesn’t tick their boxes, they might still turn you down for a mortgage. That’s where asset-based mortgages come in. Instead of focusing on your income, these mortgages consider the […]