- Can You Get a Mortgage If You Are Single?

- How Much Can I Borrow on a Single Mortgage?

- Do I Need a Bigger Deposit as a Single Applicant?

- How To Get a Mortgage as A Single Person?

- Can I Get a Mortgage if I’m Self-Employed?

- Can I Get Approved With Bad Credit?

- Can I Remortgage on My Own?

- Do You Have to Declare Dependents for a Single Mortgage?

- What Other Options Are There for Single Buyers?

- The Bottom Line

Getting a Mortgage as a Single Person: A Complete Guide

As an independent single person, you don’t need to consult another human on your life’s big decisions.

However, when buying a home alone, you might feel lost and overwhelmed by your finances.

The good news is this guide has you covered. We’ve included everything you need to know about getting a mortgage as a single person.

Can You Get a Mortgage If You Are Single?

Absolutely! While applying for a mortgage alone can seem daunting, single people can get a mortgage in the UK.

Mortgage lenders regularly grant mortgages to solo applicants – being single isn’t a barrier.

What’s important is that you meet the lender’s affordability criteria, have a good deposit, and maintain a clean credit record.

While it might be more challenging to save up for a deposit on a single income, it’s still very achievable.

When you own a home, your financial situation can often improve. Monthly mortgage payments can be lower than rental costs, giving you a chance to save more and build equity as a homeowner.

How Much Can I Borrow on a Single Mortgage?

The amount you can borrow depends on your income, credit history, deposit size, and any existing debts.

Lenders need to ensure you can comfortably afford the repayments. They will run affordability checks to stress-test the amount you want to borrow against your finances.

Each lender has different criteria, but they broadly assess:

- Your income and regular cash flow

- Your credit report and history

- Your assets and financial stability

- The size of your deposit

Use our online mortgage affordability calculator to get an estimate of your mortgage amount.

Do I Need a Bigger Deposit as a Single Applicant?

Most lenders require at least a 10% deposit for a residential mortgage, but you may be able to put down just 5% using government schemes like the Deposit Unlock Scheme or Shared Ownership.

A larger deposit means you need a smaller mortgage and can access better rates. However, don’t worry if you can’t save a large sum upfront.

Lenders need proof of where your deposit money came from, such as:

- Personal savings

- Proceeds from selling another property

- An inheritance

- A gifted deposit from family

With the right deposit proof, mortgage size, and broker advice, putting down 5-10% is absolutely achievable as a single person.

How To Get a Mortgage as A Single Person?

First, start with the basics. Have all your finances, deposits, and key documents sorted out.

Check our complete mortgage application guide to see how to prepare for a mortgage. Once sorted, you can proceed with the following:

Get an Agreement in Principle (AIP)

An AIP is a document from a lender stating how much they might lend you based on your financial situation. It gives you a clear idea of your budget and shows sellers you’re serious.

To get an AIP, provide details about your income, expenses, and credit history.

Find a Property

With your AIP in hand, start searching for a property within your budget. Consider location, property type, and future value.

Use online platforms, local estate agents, and viewings to find your ideal home.

Apply for a Mortgage

Once you’ve found a property, it’s time to apply for a mortgage.

Your lender will need information about the property and will conduct a valuation to ensure it’s worth the loan amount. Submit all necessary documents, including your AIP, proof of income, and deposit.

Exchange Contracts

After your mortgage is approved, hire a solicitor to handle the legal aspects.

They will draft and review contracts, conduct property searches, and ensure everything is in order. Exchange contracts with the seller, and pay the deposit to secure the property.

Completion

On completion day, the remaining funds are transferred from your lender to the seller. Your solicitor will finalise the legal paperwork, and you’ll receive the keys to your new home.

Congratulations, you’re now a homeowner!

If you want to speed up your process without the stress, reach out to us.

We’ll arrange a free, no-obligation consultation with a qualified mortgage broker to help you with your mortgage application.

Can I Get a Mortgage if I’m Self-Employed?

Yes, self-employed people can successfully apply for a single mortgage.

In fact, having a solid self-employed income that’s steady and easy to prove may make you more attractive to lenders than employed applicants.

Most lenders ask for 2-3 years of accounts, tax returns, and SA302 forms to evidence your earnings. But some lenders only need 1 year of accounts if you’re newly self-employed.

The key is finding a lender set up for dealing with self-employed or complex income situations.

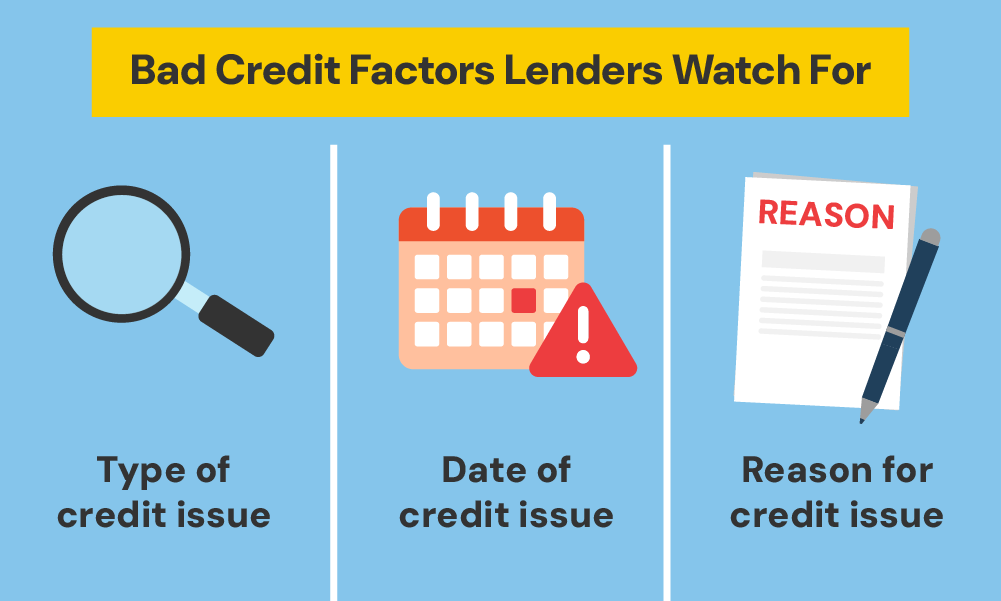

Can I Get Approved With Bad Credit?

It’s possible to get a mortgage alone even with a poor credit history, but it will be more challenging than with an excellent credit score.

Lenders are most concerned with:

- What caused your adverse credit

- How much it was for

- How long ago it occurred

- What you’ve done to improve your credit since

Older, smaller credit issues carry less weight than recent, significant problems like bankruptcies or CCJs. Be upfront about any bad credit – facing it head-on is crucial.

Start by getting your full credit report and score so you know exactly what lenders will see.

Working with a broker experienced in bad credit mortgages gives you the best chance of approval with the right lender.

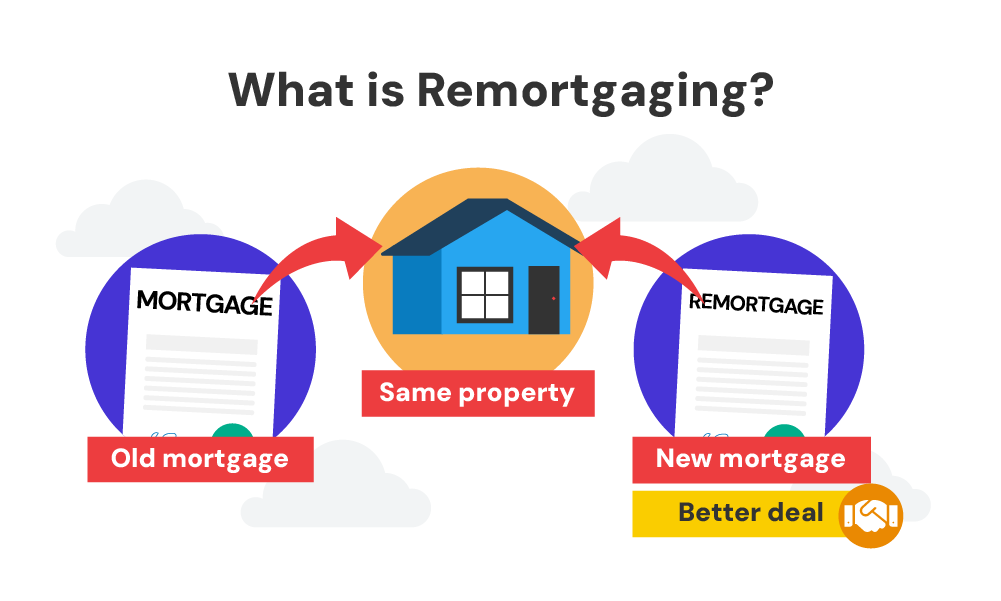

Can I Remortgage on My Own?

Yes, you can remortgage on your own. It’s similar to getting a new mortgage, but instead of buying a property, you’re borrowing against the value you’ve already built up in your existing one.

The process is straightforward. As long as you meet the lender’s criteria, you can secure a new remortgage deal.

If you’re remortgaging due to a separation, you’ll need to legally remove your ex-partner from the mortgage deed. This might involve solicitor fees, a property valuation, and potentially stamp duty.

Remember, lenders care most about your ability to repay the loan.

Do You Have to Declare Dependents for a Single Mortgage?

Yes, you need to declare any financial dependents like children when applying for a mortgage.

This could impact the amount you’re able to borrow as lenders must account for the associated costs of dependents.

However, having dependents is not an automatic barrier to getting a mortgage as a single person. The lender’s bigger concern is whether your income can cover the mortgage plus additional household costs.

Be fully honest about any dependents during your application.

What Other Options Are There for Single Buyers?

If going it completely alone seems too difficult, some other options could make homeownership more accessible:

Image showing all the alternatives to sole mortgages. Please use fewer texts.

Buying with friends/family

Pooling resources by buying a home together can make the deposit and mortgage more manageable to share.

But it’s a huge commitment – you’re all jointly responsible for payments.

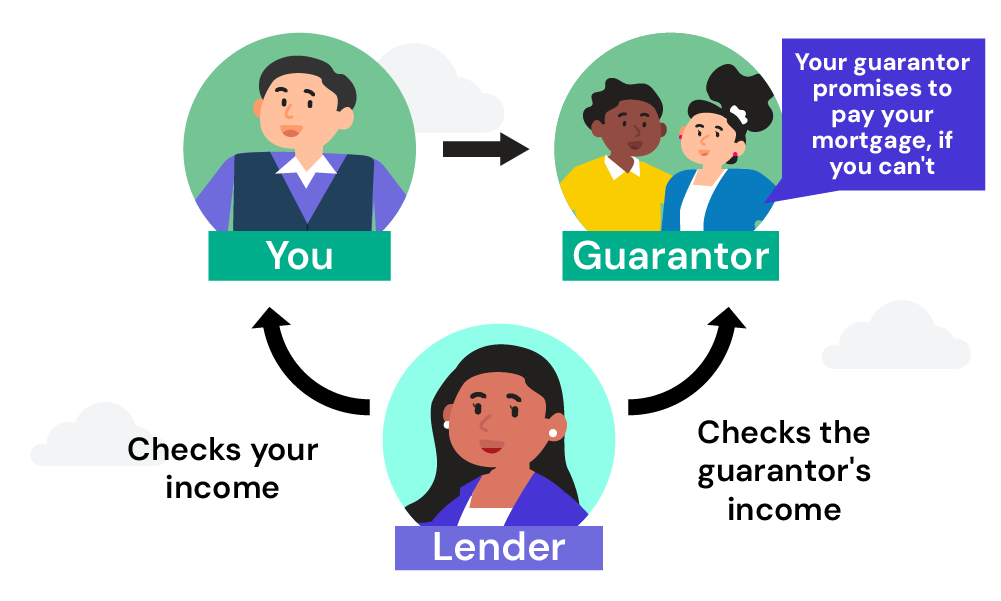

You could apply for a guarantor mortgage if struggling with affordability.

A close family member agrees to guarantee covering repayments if you can’t make them, using their own property or savings as security.

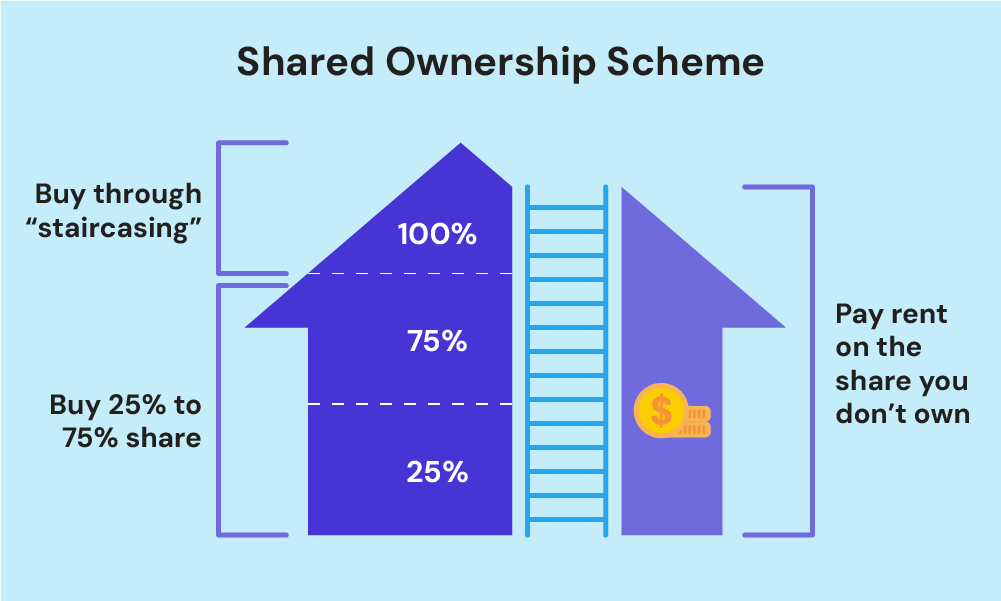

Shared Ownership

This scheme lets you buy between 25-75% of a property initially while paying rent on the remaining share. You can then increase your owned share over time through staircasing.

Right to Buy

If you’ve been a council tenant for a number of years, you may have the Right to Buy your rental home at a discount from the council.

The ideal path will depend on your specific finances and circumstances.

Speaking to an experienced mortgage broker will ensure you explore the best options for your situation as a single buyer.

The Bottom Line

Getting a mortgage alone can understandably feel overwhelming. That’s why it’s wise to work with an expert mortgage broker who has in-depth knowledge of single-applicant mortgages.

The right broker will take a huge weight off by guiding you through every step, from having the ideal documents ready to make your application look strong to underwriters.

They can identify the most suitable lenders and mortgage deals for your unique circumstances.

With an experienced broker partnering with you, your chances of getting an affordable mortgage approved as a solo buyer are much higher. Make an enquiry today to get started.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can a single person get a mortgage in Ireland?

Yes, you can. Lenders will check your income, credit history, and deposit. If affordability is an issue, government schemes like the Mortgage Guarantee Scheme, Shared Ownership, and Right to buy can help.

Can I add someone else to my sole mortgage?

Yes, you can add someone to your mortgage. You can either ask your current lender to add them or remortgage to include them. The new person will need to pass affordability and credit checks. Legal advice and potential fees may apply.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]