- What’s the Minimum Age for a Mortgage in the UK?

- Can You Get a Mortgage at 18 in the UK?

- Should You Get a Mortgage at 18?

- What Options Are Available for Young Professional Mortgages?

- How Can Young People Improve Their Chances of Getting a Mortgage?

- Government Schemes For Young People To Buy a House

- Alternatives to Traditional Mortgages for Young Buyers

- Before You Apply For a Mortgage

- Key Takeaways

- The Bottom Line

Mortgages for Young People: What You Need to Know

For many young Brits, owning a house feels like a distant dream.

Sky-high prices, hefty deposits, and that sinking feeling of rejection from lenders can make it seem out of reach.

But here’s the thing – it’s not.

Whether you’re just starting out or a working professional, there are options for you.

Government schemes, different types of mortgages, and good money habits can all help. But, it’s not always easy.

You’ll need to sort out credit scores, save for deposits, and tackle a mountain of paperwork.

But with the right know-how and a bit of planning, you could be picking out curtains for your very own place sooner than you ever imagined.

Ready?

What’s the Minimum Age for a Mortgage in the UK?

The good news is that you can legally buy a house and get a mortgage at 18.

That’s right – the moment you become an adult, you’re eligible to apply for a mortgage and purchase property.

However, it’s not quite as simple as just turning 18 and getting the keys to your new home.

While 18 is the legal age to buy a house in the UK, most lenders have their own age restrictions.

For standard residential mortgages, 18 is typically the minimum age.

But if you’re looking at buy-to-let mortgages, you might find that some lenders require you to be 21 or even 25. It’s worth noting that while you can get a mortgage at 18, it can be challenging.

Lenders want to see a solid credit history and financial stability, which many 18-year-olds haven’t had the chance to establish yet.

But don’t let that discourage you – with the right preparation and guidance, it’s entirely possible to get on the property ladder at a young age.

Can You Get a Mortgage at 18 in the UK?

Yes, you can get a mortgage at 18 in the UK, but it’s not without its challenges.

At 18, you’re likely just starting your career, and you may not have had the opportunity to build up a substantial credit history.

These factors can make lenders hesitant to offer you a mortgage.

However, it’s not impossible.

There are things you can do to increase your chances of approval such as saving up more deposit, building credit, or increasing your income – we’ll talk more about this later.

Should You Get a Mortgage at 18?

Getting a mortgage at 18 is a big decision. It can set you on a path to homeownership early in life, but it also comes with challenges.

Here are the pros and cons to help you decide if it’s the right move for you:

Pros:

- You start building equity early, giving you a head start in the property market.

- Your monthly payments might be lower than renting, saving you money in the long run.

- Owning your home gives you financial independence and stability.

- You can take advantage of government schemes designed for first-time buyers.

- Over time, your property’s value could increase, boosting your wealth.

Cons:

- With a limited credit history, getting good mortgage terms might be tougher.

- You’ll have less flexibility to move or travel compared to renting.

- You’ll be responsible for maintenance and unexpected repairs.

- Committing to long-term debt at a young age can be overwhelming.

- If your income is unstable or low, you might struggle to keep up with payments.

What Options Are Available for Young Professional Mortgages?

If you’re a young professional looking to buy a home, you might be pleased to know that some lenders offer special mortgage products tailored to your situation.

These young professional mortgages often come with more favourable terms, recognising that while you might be early in your career, you have strong earning potential.

Lenders typically define ‘young professionals‘ as those under 35 in certain professions, such as doctors, lawyers, accountants, or engineers.

The benefits of these mortgages can include:

- Higher loan-to-income ratios. Some lenders might offer up to 5.5 times your income, compared to the standard 4.5.

- Lower deposit requirements. You might be able to get a mortgage with just a 5% deposit.

- Exclusion of student loan debt. Some lenders might not factor in your student loan when calculating affordability.

- Consideration of future earning potential. If you’re in a profession with clear career progression, lenders might take this into account.

To qualify for a young professional mortgage, you’ll typically need to be qualified and practising in your profession.

It’s worth shopping around and speaking to a mortgage broker who can help you find lenders offering these specialist products.

How Can Young People Improve Their Chances of Getting a Mortgage?

Getting a mortgage as a young person can be challenging, but there are several steps you can take to improve your chances:

- Save for a bigger deposit – The more you can put down, the better your chances of approval and the better rates you’ll be offered. Aim to save at least 10% of the home’s value.

- Build your credit score – This is crucial. Make sure you’re on the electoral roll, pay bills on time, and consider getting a credit builder credit card to establish a positive credit history.

- Reduce existing debts – Pay off any outstanding loans or credit card balances to improve your debt-to-income ratio.

- Maintain stable employment – Lenders like to see a steady income, so try to stay in the same job for at least 6 months before applying.

- Be realistic about what you can afford – Don’t overstretch yourself – lenders will look closely at your income and outgoings.

- Consider government schemes – Look into options like Mortgage Guarantee Scheme, Shared Ownership, or Lifetime ISAs which can make homeownership more accessible.

- Get professional advice – A qualified mortgage broker can guide you through the process and help you find lenders more likely to approve your application.

Remember, improving your mortgage chances is a process.

If you’re not ready now, use this time to prepare so you’re in a stronger position when you do apply.

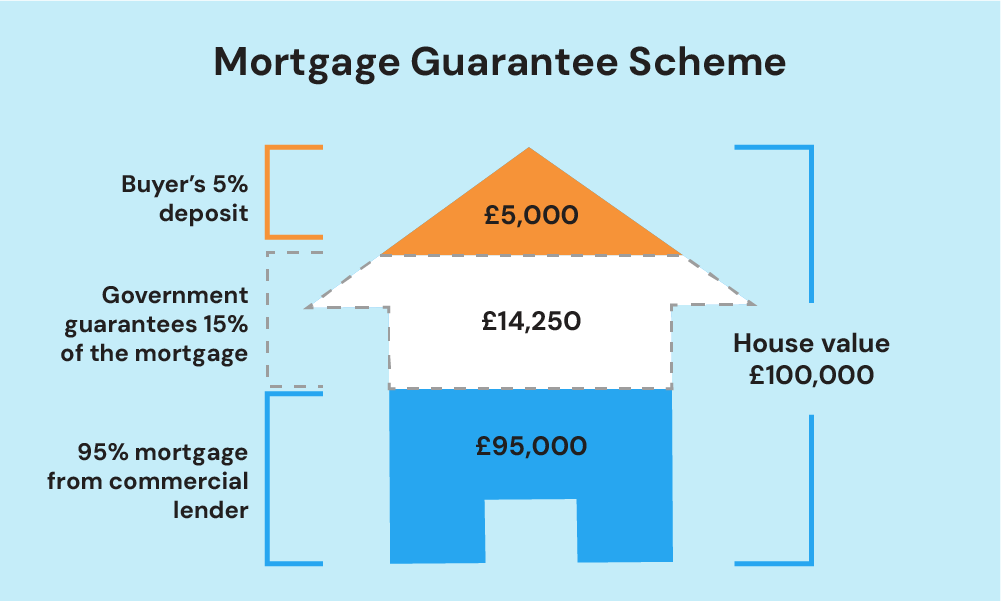

Government Schemes For Young People To Buy a House

The UK government offers several schemes designed to help young people and first-time buyers get on the property ladder. Here are some options you might want to consider:

- Shared Ownership – This allows you to buy a share of a property (between 25% and 75%) and pay rent on the rest. You can buy bigger shares when you can afford to.

- Lifetime ISA – If you’re 18-39, you can save up to £4,000 a year into this ISA, and the government will add a 25% bonus to your savings, up to a maximum of £1,000 per year.

- First Homes Scheme – This offers a discount of 30% to 50% on the market price of new-build homes for first-time buyers.

- Mortgage Guarantee Scheme – This helps first-time buyers get a mortgage with just a 5% deposit, with the government acting as a guarantor for part of the mortgage. Be aware that this scheme is set to close for new applications at June 2025.

These schemes can make a difference in helping young people afford their first home. It’s important to do your research and get professional advice before deciding which, if any, is right for you.

Alternatives to Traditional Mortgages for Young Buyers

Struggling to get a traditional mortgage? Here are alternatives you might want to consider:

- Guarantor mortgages – A parent or close family member agrees to cover the mortgage payments if you can’t. This can help you get approved with a smaller deposit or lower income.

- Family offset mortgages – Your family can put their savings into an account linked to your mortgage, reducing the amount of interest you pay.

- Joint mortgages – You could buy with a friend or family member, combining your income and deposits to afford a more expensive property.

- Rent to Buy schemes – These allow you to rent a property for a set period with the option to buy it later, often at a discounted price.

- Family springboard mortgages – Similar to a guarantor mortgage, but your family’s savings are held as security instead of their property.

These schemes might make buying a home easier, but they also involve risks. You should fully understand the terms and consequences before committing.

Before You Apply For a Mortgage

Applying for a mortgage can seem daunting, especially if you’re young and it’s your first time.

Here’s what you need to know:

- Sort Out Your Money. Look at how much money you make, spend, and save. It’s important to know where you stand. Start saving for a deposit and try to pay off any debts to help improve your credit score.

- Check Your Credit Report. Get a copy of your credit report and check it for any mistakes. Fix anything that could hurt your chances of getting a mortgage. Try to keep your credit card balances low and avoid applying for new credit before you apply for a mortgage.

- Collect Your Papers. Gather important documents like your recent payslips, bank statements, ID, and proof of where you live. If you’re self-employed, you’ll need your tax returns and business records.

- See How Much You Can Borrow. Use an online mortgage calculator to figure out how much you might be able to borrow. This will help you know what kind of houses you can afford.

- Get a Mortgage in Principle. This is a statement from a lender saying how much they might lend you. It’s not a final offer, but it can help you when making offers on a house.

- Use a Mortgage Broker. A mortgage broker can help you find the best deals and handle the paperwork for you. They also talk to lenders on your behalf, making things easier.

In the months before your application, avoid applying for other credit. It can impact your score. And be patient – applications can take 2-3 months.

If you’re rejected, ask why, fix the issues, and try again with a new lender.

Getting a mortgage is a big step. Take your time, do your research, and don’t hesitate to ask for help or advice.

Key Takeaways

- You can apply for a mortgage at 18 in the UK, but lenders prefer strong credit and stable finances.

- Young professionals can access special mortgages with better terms, like higher loan limits and lower deposits.

- Improve your chances by saving more, building credit, reducing debts, and keeping a steady job.

- Government schemes and other mortgage options can make buying a home more affordable.

The Bottom Line

Buying your first home as a young person can be challenging. With so much information and so many options, it’s easy to feel lost.

You also worry about missing out on the perfect place.

A good mortgage broker can simplify the process. They’ll help you find the best deals, offer a wider choice of mortgages, and guide you through the paperwork.

With their expertise, you can overcome challenges and increase your chances of getting the home you want.

So, take a deep breath, plan ahead, and remember – your dream home is within reach.

Want to make things easier? Get in touch with us. We’ll connect you with a qualified mortgage broker who can help with your mortgage application.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

At what age can I buy land in the UK?

In the UK, you must be at least 18 years old to legally buy land. This is because, at 18, you are considered an adult and can enter into binding contracts, including property transactions.

What is the youngest age you can own a property in the UK?

The youngest age you can own property in the UK is 18. While minors (those under 18) can technically own property, they cannot hold legal title in their name.

Instead, the property would need to be held in trust by a legal guardian or trustee until they reach the age of 18.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

What Stops You Getting a Mortgage? 9 Key Factors to Know

Securing a mortgage isn’t always easy. Some people find it tough to save for a deposit. Others struggle to find lenders with flexible terms. Many face challenges with their credit score. These things can get in your way. But don’t worry – knowing what they are is the first step to beating them. To help […]

Tier 2 Visa Mortgages: What You Need to Know

If you’re a foreigner planning to settle in the UK long-term, buying a home is probably on your wish list. But let’s be real: getting a mortgage here isn’t easy, especially if you’re on a Tier 2 visa. Limited credit history, short residency, and the need for a large deposit makes it tough for you […]

How To Transfer, Add, Or Remove Names On A Joint Mortgage?

When you’re buying a home with someone else, you might opt for a joint mortgage. This means you’re both responsible for the loan. It’s common among couples, friends, or family members pooling resources to buy property. But what happens when circumstances change? Can you alter who’s on the mortgage? In this guide, we’ll explain all […]