- Is It Possible for a Lender to Withdraw a Mortgage Offer?

- What Are the Primary Reasons for Mortgage Offer Withdrawal?

- At What Stage Can a Mortgage Offer Be Withdrawn?

- Can a Mortgage Offer Be Withdrawn on the Day of Completion?

- What Steps Should You Take If Your Mortgage Offer Is Withdrawn?

- The Bottom Line

What Should I Do If My Mortgage Declined After Exchange?

Buying a home is a big step. It’s exciting, but it also comes with a lot of important decisions.

One of these is getting a mortgage – a key part of making your dream home a reality.

When you apply for a mortgage and get that offer from the lender, it feels like you’re on the right track. But, it’s crucial to know that sometimes, even after you’ve received a mortgage offer, things can change.

In some rare cases, a lender might withdraw their mortgage offer.

This doesn’t happen often, but when it does, it can be confusing and disappointing.

This guide is here to walk you through what this means, why it might happen, and how it can affect your journey to becoming a homeowner.

Is It Possible for a Lender to Withdraw a Mortgage Offer?

Yes, lenders have the right to withdraw a mortgage offer. This can happen at any point before the completion of the loan.

While not common, there are specific reasons why a lender might decide to retract an offer. These include significant changes in your financial circumstances, such as losing your job, or if inaccuracies are discovered in the information you’ve provided.

Issues with the property, like a negative valuation or legal problems, can also lead to offer withdrawal. Lenders make these decisions based on risk assessments and the feasibility of the loan, ensuring both your and their interests are protected.

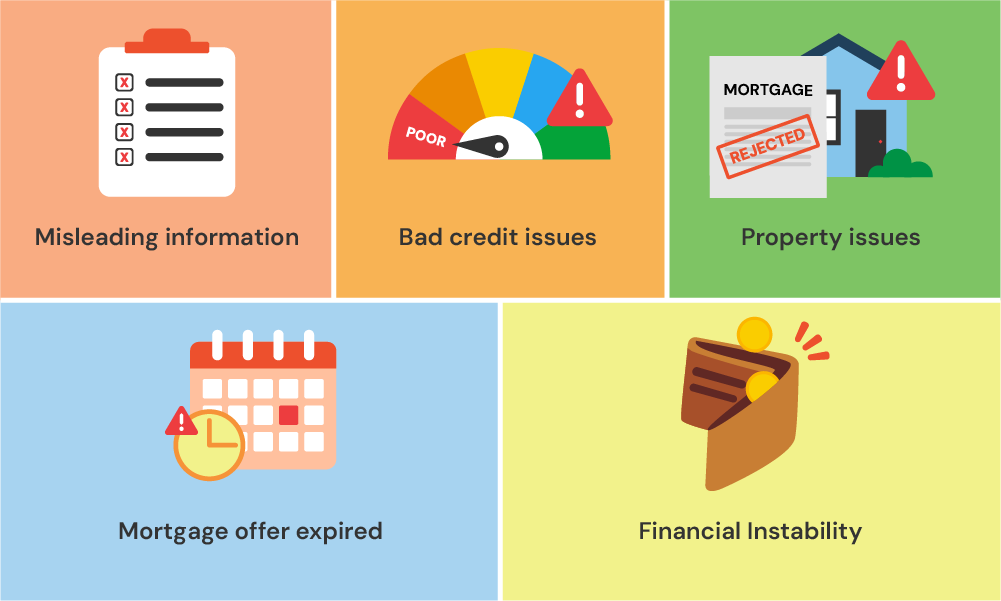

What Are the Primary Reasons for Mortgage Offer Withdrawal?

When you get a mortgage offer, it’s a big step towards buying your home. But sometimes, a lender might need to withdraw this offer.

Let’s look at the main reasons why this can happen.

Expiry of the Mortgage Offer

Every mortgage offer comes with a ‘use-by’ date. Typically, this is around 3 to 6 months.

If you don’t complete the purchase within this time, the lender might withdraw the offer. It’s like a loaf of bread that has a best-before date. If you don’t use it in time, it’s no longer good.

Changes in Your Financial Situation

If your money situation changes after you get the offer, the lender will need to review it.

For example, if you lose your job or if you suddenly have a lot more bills to pay, the lender might think you won’t be able to pay back the mortgage. They need to make sure you can still afford the repayments.

Discovery of Suspicious Activities or Inaccuracies

If the lender finds out that some information you gave them isn’t true, they might withdraw the offer.

It’s like playing a game fairly – if you don’t play by the rules, you can’t keep playing. They check for things like incorrect income details or misleading information about your debts.

Credit Issues Arising After-Offer

After you get a mortgage offer, the lender might check your credit again.

If they find new problems with your credit report, like missed payments or more debts, they might reconsider the offer. It’s like they’re making sure your financial health is still good.

Problems Identified with the Property Being Purchased

Sometimes, issues come up with the property you’re buying. This could be a lower-than-expected value or legal problems with the property’s title.

If the lender thinks the property isn’t a safe investment, they might pull back the offer. It’s like double-checking that the house is worth the money they’re lending.

Remember, these reasons are about making sure the loan is safe for both you and the lender. It’s important to keep all your information up to date and be honest with your lender to avoid these issues.

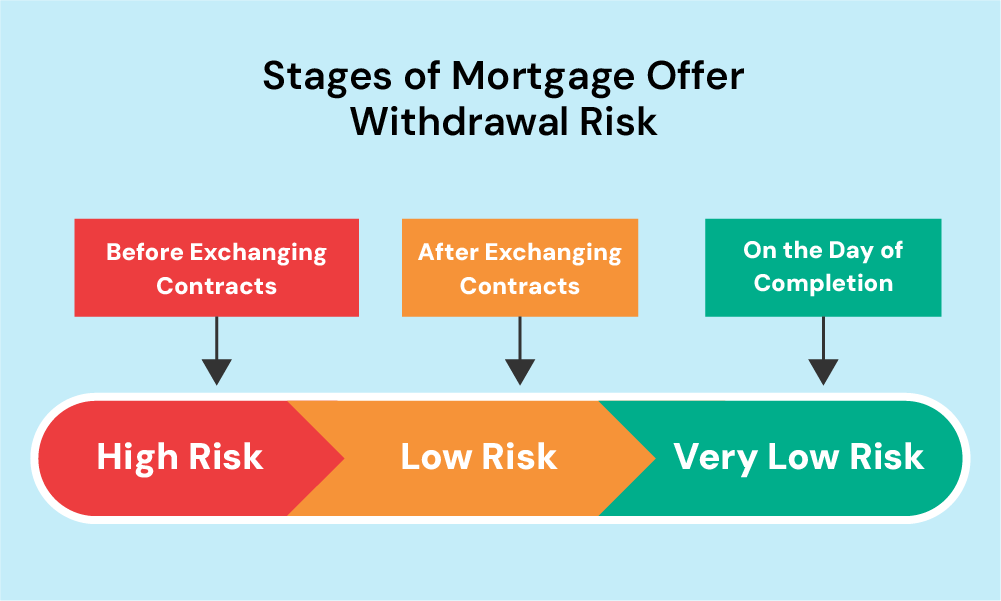

At What Stage Can a Mortgage Offer Be Withdrawn?

A mortgage offer can be withdrawn at different times during the home-buying process. The risk of this happening changes depending on the stage you’re at.

Before Exchanging Contracts

This is the early stage where you’re just agreeing to buy the house. Here, the risk of an offer being withdrawn is higher.

Why? Because everything is still up in the air. Your financial situation could change, or the lender might find something in your application that needs a closer look.

It’s a bit like being on a trial period – things aren’t set in stone yet.

After Exchanging Contracts

Once you exchange contracts with the seller, the deal becomes more solid. But, there’s still a small chance of the offer being pulled back.

If something major changes with your finances or if the lender spots a big problem, they might need to rethink the offer. It’s rarer at this stage, but it’s still possible.

On the Day of Completion

In very rare cases, a mortgage offer can be withdrawn on the day of completion if critical issues are identified last minute.

The main thing to remember is, that the closer you get to completing the purchase, the less likely it is that your mortgage offer will be withdrawn. Keeping things consistent and stable in your finances during this time is key.

Can a Mortgage Offer Be Withdrawn on the Day of Completion?

As discussed earlier, a mortgage offer can rarely be withdrawn on the day of completion. This is the final stage where the transaction is completed, and you are set to become the owner of your new home.

A mortgage offer might be withdrawn at this stage due to sudden and significant issues, such as a major problem discovered in your credit report or a legal complication with the property. These are serious concerns that can compel the lender to revoke the offer.

The financial and legal implications of such a last-minute withdrawal are significant. It can lead to the loss of various fees you have already paid, including those for surveys and legal services.

Legally, you might also lose your deposit and face other penalties. In this scenario, you could find yourself bearing financial losses and, unfortunately, without the property.

What Steps Should You Take If Your Mortgage Offer Is Withdrawn?

Finding out your mortgage offer has been withdrawn can be stressful, but there are steps you can take to handle the situation.

First, don’t panic.

Contact your lender straight away to understand why the offer was withdrawn. It’s important to get clear information on what’s happened. Maybe it’s a problem that can be sorted out quickly.

Next, it might be a good idea to talk to a legal or mortgage advisor. They can help you understand your options and what to do next.

If the issue is with your credit, they can advise you on how to fix it. If it’s a problem with the property, they might help you negotiate with the seller or find another solution.

If the issue can’t be resolved quickly, you may need to start looking for other mortgage options. This is where a mortgage broker can be really helpful. They can find lenders who might be more suitable for your situation.

Remember, communication is key. Keep in touch with your lender, your legal advisor, and your estate agent. They’re all there to help you get through this and find the best way forward.

The Bottom Line

In this guide, we’ve explored the complexities surrounding the withdrawal of mortgage offers. It’s a situation that can be stressful, but understanding why it happens and how to respond is key.

Here’s where a mortgage broker can make a difference.

Mortgage brokers are experts in the field of home loans. They know the ins and outs of various mortgage products and the criteria different lenders have.

If your mortgage offer gets withdrawn, a broker can be your best ally. They can review your situation, advise on the next steps, and help you find alternative mortgage options that fit your circumstances. They take on the heavy lifting of comparing different mortgages, saving you time and effort.

With their knowledge and connections, brokers can find solutions that you might not have considered or had access to. They can also assist in smoothing out any issues that led to the withdrawal of your offer, be it problems with your credit history or the property itself.

If you’re facing a withdrawn mortgage offer and need expert guidance, don’t hesitate to get in touch with us. We can connect you with an FCA-qualified broker who will help you navigate your specific mortgage situation, saving you time and stress.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can banks withdraw a mortgage offer after the exchange?

Yes, banks can withdraw a mortgage offer even after the exchange of contracts, although it’s quite rare.

This might happen if there are significant changes in your financial situation, such as losing your job or taking on substantial new debt, which could affect your ability to repay the mortgage.

Other reasons include discovering inaccuracies or fraud in the application, sudden issues with the property’s value, or legal problems.

It’s important to maintain open communication with your bank and update them on any major changes to your circumstances to reduce the risk of this happening.

Is it possible for a mortgage to be cancelled after completion?

Once your property purchase is finalised, your mortgage can’t be cancelled. However, if you don’t keep up with payments or violate your mortgage terms, the lender might start legal proceedings.

To prevent losing your home, keep in touch with your lender if you face financial difficulties. Short-term solutions like payment holidays or extending your mortgage term might be available, so it’s key to raise any issues early.

What are the chances of a mortgage offer being cancelled?

Generally, lenders are reluctant to cancel mortgage offers and usually do so only as a last option. If you inform them promptly about any mistakes or changes in your situation, they often prefer to modify the mortgage terms or adjust your loan amount instead.

Can my mortgage offer be cancelled due to suspension or furlough?

Being furloughed could lead to your mortgage offer being put on pause, especially if there are doubts about your job stability or ability to afford the mortgage long-term.

With many affected by pandemic-related furloughs, several lenders have adjusted their criteria. If your offer is withdrawn, a broker might direct you to lenders who are more accommodating towards furloughed individuals.

Will redundancy affect my mortgage offer?

Yes, redundancy can influence your financial stability, prompting lenders to reconsider your mortgage offer. However, if redundancy doesn’t significantly affect your ability to afford the mortgage – like having another income source or applying jointly – lenders might still approve your mortgage after revising the terms.

Can I cancel my mortgage application?

You’re free to cancel your mortgage application at any stage before completion, even after submitting all documents.

Note that any fees paid are usually non-refundable, and there might be additional costs depending on your application stage. If you’re uncertain about the mortgage or your repayment capability, it’s wise to discuss with your lender or consult a broker before making a decision.

Related Articles

A Complete Guide To Mortgages Refused Due To Flood Risk

If you’ve ever thought about buying a home in the UK, you’ll know it’s not all about cute cottages and lovely gardens. There are a few extra challenges, like the weather. And by weather, we mean rain – lots of it. That lovely drizzle we Brits love to grumble about can sometimes lead to flooding, […]

Mortgage Approvals & Rejections: What You Need to Know

Getting a mortgage can feel like a rollercoaster ride. You’ve found your dream home, pictured yourself settled in, but then—bam! The dreaded rejection email comes through, and suddenly it feels like everything’s on hold. But don’t worry; you’re not alone in this experience. Mortgage rejections happen more often than you think, and while it’s frustrating, […]

What Should I Do If Skipton Refused My Mortgage?

Are Skipton Building Society Strict? Skipton Building Society’s mortgage lending criteria are quite comparable to other major UK lenders. They focus on essential factors such as your credit history, income, and the type of property you’re looking to buy. If you’re applying for a mortgage with them, it’s important to have a clear credit record […]