- Why Might Halifax Decline a Mortgage Application?

- How Long Does It Take for Halifax to Process a Mortgage Application?

- What Should You Do If Halifax Declines Your Mortgage Application?

- Is Challenging Halifaxâs Mortgage Decision an Option?

- Common Grounds for Halifax Declining Mortgage Applications

- How Long Should You Wait Before Reapplying for a Mortgage?

- The Bottom Line

What To Do If Halifax Refused Your Mortgage Application?

Being turned down for a mortgage can be disheartening, especially when you’ve set your sights on a home that feels just right for you.

If you’ve recently experienced a refusal from Halifax, you’re not alone. Many face this hurdle in their journey to homeownership.

In this guide, we’ll delve into the reasons behind Halifax’s mortgage decisions and provide you with insights to help you navigate this challenge.

Why Might Halifax Decline a Mortgage Application?

Halifax, like all major lenders on the high street, has a set of guidelines they follow when reviewing mortgage applications. These rules are in place to ensure they lend responsibly.

However, Halifax is also recognised for its accommodating stance towards a variety of borrowers, including those buying their first home, individuals with a lower income, or those who have had some credit hiccups.

It’s important to note that while Halifax is flexible, there are specialist lenders in the market who may offer more bespoke solutions, especially for unique or complex financial situations.

A mortgage broker can be invaluable in these instances, helping to match your needs with a lender who can cater to your specific situation.

How Long Does It Take for Halifax to Process a Mortgage Application?

Generally, Halifax suggests that the process can take up to three months. This is just a rough guide, though. The actual time can vary based on several factors.

Several things can affect how long it takes for Halifax to approve your mortgage. These include how quickly you can provide all the necessary documents, the complexity of your financial situation, and how busy they are at the time.

Also, if there are any issues with the property you’re buying – like legal problems or valuation concerns – this can add time to the process.

It’s a bit like putting together a jigsaw puzzle; the more pieces there are, the longer it can take.

What Should You Do If Halifax Declines Your Mortgage Application?

Being declined for a mortgage by Halifax can feel like a setback, but it’s not the end of the road. Here’s what you should do:

Don’t Rush into Another Application

It’s tempting to try another lender immediately, but it’s better to pause and reflect first.

Applying too quickly to another lender might harm your credit score, especially if you’re not sure why Halifax declined you.

Understand Why Your Application Was Declined

The key is to find out why Halifax said no. They should provide you with a reason, and this information is gold dust.

It could be something about your financial situation, or maybe there’s an issue with the property you’re looking to buy. Knowing the reason helps you to fix the problem before you apply again.

In both cases, taking a considered approach helps you to strengthen your application for the next time around. It’s about learning, adjusting, and then moving forward with a better chance of success.

Is Challenging Halifax’s Mortgage Decision an Option?

Yes, it’s possible to appeal a mortgage rejection from Halifax, but it’s important to know when and how this can work.

Firstly, an appeal could be successful if there’s been a misunderstanding or if Halifax based its decision on incorrect or outdated information.

For example, if your financial situation has recently improved but this wasn’t reflected in the information Halifax had, an appeal might change their decision.

To start an appeal, you should contact Halifax directly.

Explain clearly why you believe their decision should be reconsidered. It’s helpful to provide any new evidence or information that supports your case. This could include updated bank statements, new employment details, or corrected credit reports.

Remember, an appeal is about presenting new or corrected information that Halifax didn’t consider initially.

Simply disagreeing with their decision, without providing new evidence, is unlikely to change the outcome.

Appealing a mortgage decision requires a clear understanding of why the application was declined in the first place.

If you’re not sure, it’s a good idea to ask Halifax for a detailed explanation. This will help you address the specific issues that led to the rejection of your appeal.

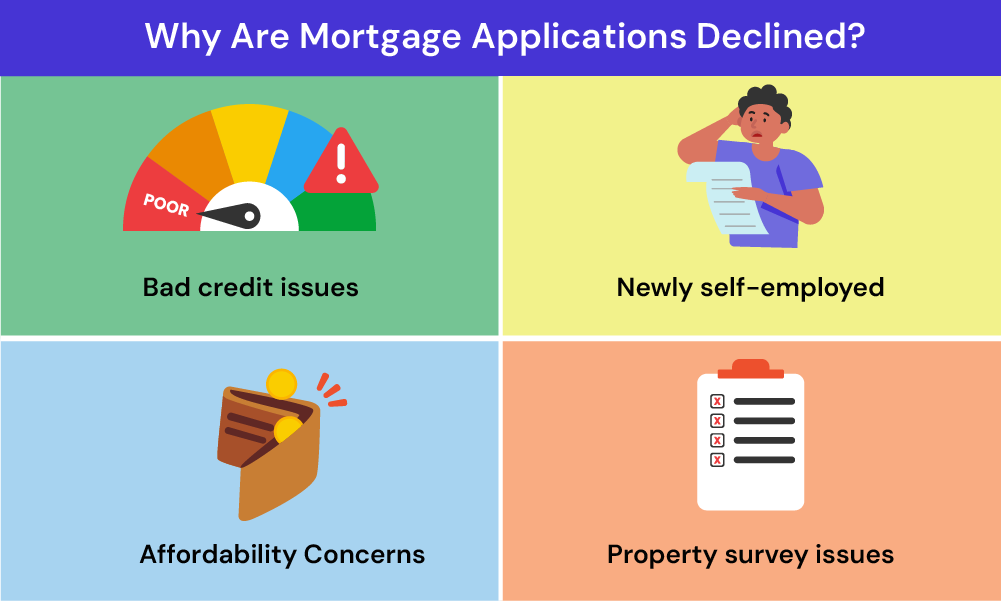

Common Grounds for Halifax Declining Mortgage Applications

When Halifax turns down a mortgage application, it’s usually for specific reasons. Here are some of the most common grounds for rejection by Halifax:

Credit Issues Discovered During Underwriting

Your credit history plays a big part in mortgage approval. During the underwriting process, Halifax examines your credit report in detail.

If they find issues like missed payments, high levels of existing debt, or other red flags, it could lead to a rejection. It’s crucial to check your credit report for accuracy before applying.

Challenges for Newly Self-Employed Applicants

If you’ve recently become self-employed, Halifax might be cautious. They typically look for a stable income history, often preferring applicants to have at least two years of self-employment records. This is to ensure that your income is reliable and consistent.

Affordability Concerns

Halifax assesses whether you can afford the mortgage based on your income and outgoings. They use a calculation based on income multiples and consider your other financial commitments.

If they think the mortgage payments might be too much for you to handle comfortably, they might not approve your application.

Issues Identified During Property Surveys

Sometimes, problems are found with the property you want to buy. This could be structural issues, legal concerns, or other factors that affect the property’s value or safety.

If such problems are significant, they could lead to Halifax declining your application.

Other Specific Reasons

Other factors might influence Halifax’s decision. This includes your employment status (if it’s unstable or if you’ve recently changed jobs), the size of your deposit (a smaller deposit can be riskier for the lender), and the type of property you’re buying (some lenders have restrictions on property types).

If you’re aware of any issues like these, it’s a good idea to address them before applying for a mortgage.

This could involve improving your credit score, waiting until you have a longer history of self-employment, or reassessing your budget to ensure the mortgage is affordable for you.

How Long Should You Wait Before Reapplying for a Mortgage?

Deciding when to reapply for a mortgage after being declined by Halifax depends on fixing the issues that caused the initial rejection.

There’s no one-size-fits-all answer, but here’s some guidance:

If your application was declined due to credit issues, take time to improve your credit score.

This might involve paying off debts, ensuring all bills are paid on time, and possibly waiting for negative marks to age off your credit report. This process can take several months to a year, depending on your specific credit issues.

In cases of affordability concerns or being newly self-employed, you might need to wait until your financial situation has stabilised or improved.

This could mean waiting for a more consistent income flow or reducing your outgoings to improve your debt-to-income ratio.

For issues related to the property, such as valuation problems or structural issues, you may reapply sooner, possibly with a different property in mind or once the issues with the initial property are resolved.

In general, it’s wise to wait until you’ve adequately addressed the reasons for the initial rejection.

Rushing into another application without making necessary changes is unlikely to yield a different result.

The Bottom Line

Throughout this guide, we’ve covered the key aspects of understanding and dealing with a mortgage application refusal from Halifax. From identifying the common reasons for rejection to considering the best time to reapply, it’s clear that a thoughtful approach is crucial.

Mortgage brokers can be invaluable in these situations. They have the expertise to guide you through the application process, help you understand the lender’s requirements, and find a mortgage product that suits your circumstances.

Brokers can also assist in renegotiations with lenders or identify alternative lending options that you might not have considered.

If you’re feeling overwhelmed by the mortgage application process or need guidance after a rejection, don’t hesitate to reach out for professional help.

Contact us, and we’ll connect you with an FCA-qualified broker who can assist you in resolving your specific mortgage issues, saving you time and reducing stress in your home-buying journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently Asked Questions

Find answers to common questions here.

What are Halifax’s credit score requirements for mortgage approval?

Halifax doesn’t disclose a specific credit score requirement for mortgage approvals. Instead, they assess each application on a case-by-case basis, considering various factors.

These include your credit history, income, outgoings, and the property’s value. A higher credit score certainly improves your chances, but Halifax also considers the overall financial picture when making its decision.

Can I use income from gambling for a Halifax mortgage application?

When applying for a mortgage with Halifax, income from gambling is generally not considered a stable or reliable source.

Halifax, like most lenders, looks for consistent and predictable income when assessing mortgage applications. If your main income is from gambling, it may be challenging to get approval.

However, if gambling is a secondary income source and you have a stable primary income, you might still be considered.

Does the property's valuation affect my mortgage approval with Halifax?

Yes, the valuation of the property you wish to purchase plays a crucial role in your mortgage approval.

Halifax needs to ensure the property is worth the amount you wish to borrow. If the valuation is lower than expected, it could affect the loan amount Halifax is willing to offer or even lead to a decline of your application.

This is because the property is used as security against your mortgage.

What are Halifax’s credit check procedures after making a mortgage offer?

Once Halifax makes a mortgage offer, they have usually completed their credit checks. However, it’s important to maintain a good credit standing throughout the process.

Halifax might conduct additional checks if there’s a significant delay between the offer and completion or if they receive new information that warrants a review.

Related Articles

A Complete Guide To Mortgages Refused Due To Flood Risk

If you’ve ever thought about buying a home in the UK, you’ll know it’s not all about cute cottages and lovely gardens. There are a few extra challenges, like the weather. And by weather, we mean rain – lots of it. That lovely drizzle we Brits love to grumble about can sometimes lead to flooding, […]

Mortgage Approvals & Rejections: What You Need to Know

Getting a mortgage can feel like a rollercoaster ride. You’ve found your dream home, pictured yourself settled in, but then—bam! The dreaded rejection email comes through, and suddenly it feels like everything’s on hold. But don’t worry; you’re not alone in this experience. Mortgage rejections happen more often than you think, and while it’s frustrating, […]

What Should I Do If Skipton Refused My Mortgage?

Are Skipton Building Society Strict? Skipton Building Society’s mortgage lending criteria are quite comparable to other major UK lenders. They focus on essential factors such as your credit history, income, and the type of property you’re looking to buy. If you’re applying for a mortgage with them, it’s important to have a clear credit record […]