- What is a Self-Employed Buy to Let Mortgage?

- Can You Get a Buy to Let Mortgage When Self-Employed?

- Eligibility Criteria for Self-Employed Buy-to-Let Mortgages

- How Much Deposit Do You Need for a Self-Employed Buy-to-Let Mortgage?

- How Much Can You Borrow?

- Which Lenders Offer Buy to Let Mortgages for Self-Employed?

- Remortgaging a Buy-to-Let Mortgage

- Key Takeaways

- The Bottom Line: Your Next Steps

How To Get Buy To Let Mortgages As Self-Employed?

Getting a buy-to-let mortgage when you’re self-employed takes a bit more effort, but it’s far from impossible.

While lenders ask for extra proof of income, plenty of them are willing to work with self-employed borrowers.

You just need to know what they’re looking for and how to meet their criteria.

This article will break down the challenges, explain how to overcome them, and help you get closer to securing that investment property.

Whether you’re a first-time landlord or expanding your portfolio, you’ll learn exactly what it takes to get approved—without the hassle.

What is a Self-Employed Buy to Let Mortgage?

The term “self-employed buy-to-let mortgage” does not refer to a specific product tailored for self-employed individuals.

Buy-to-let mortgages are essentially the same, whether you’re self-employed or in regular employment.

However, self-employed applicants are evaluated differently by lenders. Because you are the head of your own business, lenders may perceive a higher risk in lending you money.

But don’t let this discourage you. While the assessment process may be more cautious, there is good news.

Some lenders specialize in working with self-employed individuals, and others may have no strict income requirements at all, making it easier to get approved for a mortgage.

Here are some of the factors that lenders will consider when assessing a self-employed buy-to-let mortgage application:

- Your personal income

- Your business income

- Your credit history

- Your financial reserves

- Your experience as a landlord

- The property you are buying

If you are self-employed and thinking about getting a buy-to-let mortgage, it’s important to speak to a mortgage broker who can help you understand your options and find the best lender for you.

Can You Get a Buy to Let Mortgage When Self-Employed?

Yes, you can.

Being self-employed, you might think that your options are limited, especially if your income is wrapped up within your business.

But the landscape of buy to let mortgages is more accommodating than you might think.

Even a small profit in your accounts, say £200, can be seen as income by lenders. Since some of them have no minimum income requirements, this seemingly small amount doesn’t pose an issue.

If you have previous experience in owning buy to let property, lenders will even consider you as a lesser risk, allowing you to secure a mortgage even without a regular income.

The logic behind this is quite simple: the rent you receive will generally cover the mortgage payments, providing a consistent monthly profit.

Therefore, lenders are often willing to overlook traditional income sources, focusing instead on the rent’s ability to meet the mortgage obligations.

And since many buy to let mortgages operate on interest-only rates, your monthly payments can remain attractively low.

Eligibility Criteria for Self-Employed Buy-to-Let Mortgages

If you’re self-employed and considering investing in a buy-to-let property, you might be wondering what criteria lenders will look at to assess your eligibility.

It’s not just about income. Lenders take a comprehensive view that includes experience, credit history, and the type of property you’re interested in.

Here’s a closer look at the main factors:

Income Statements

You’ll need to show at least one to three years of accounts to prove your financial stability.

Usually, a certified or chartered accountant must verify these. It’s a crucial step for lenders to understand your financial footing.

Landlord Experience

Have you been a landlord before? If so, this experience could work in your favour.

Some lenders may even overlook strict income requirements, seeing your past success as evidence that you can handle a buy-to-let property.

Credit History

Your credit score matters just as much as it would if you were not self-employed.

A good credit history can lead to more competitive mortgage options, so keeping your finances in check is essential.

Property Type and Location

The type of property you’re interested in and its location can influence lender decisions.

Certain lenders might prefer properties in specific areas or be more cautious with particular types, such as Houses in Multiple Occupation (HMOs). Your property choice can affect the range of lenders available to you.

Keep in mind that the criteria mentioned above are typical for self-employed buy-to-let mortgages, but they might differ based on the lender or your specific situation.

It’s a good idea to chat with a mortgage advisor or lender to get the details that apply to you.

How Much Deposit Do You Need for a Self-Employed Buy-to-Let Mortgage?

If you’re self-employed, you’ll generally need at least a 25% deposit. That’s based on a 75% Loan to Value (LTV) ratio, which is a common starting point.

But what if you can’t quite make 25%?

Some lenders might accept a little less, like 15-20%, especially if your self-employed finances are in good shape.

But aiming for 25% or more is wise, as it often means you’ll get a better interest rate.

Putting it simply, the more you can save for the deposit, the better your mortgage deal is likely to be.

Whether you’re just starting out as self-employed or have been your own boss for years, knowing the deposit requirement helps you plan ahead.

If you can go higher than 25%, it might be worth it. It’s about understanding the numbers and what works best for you.

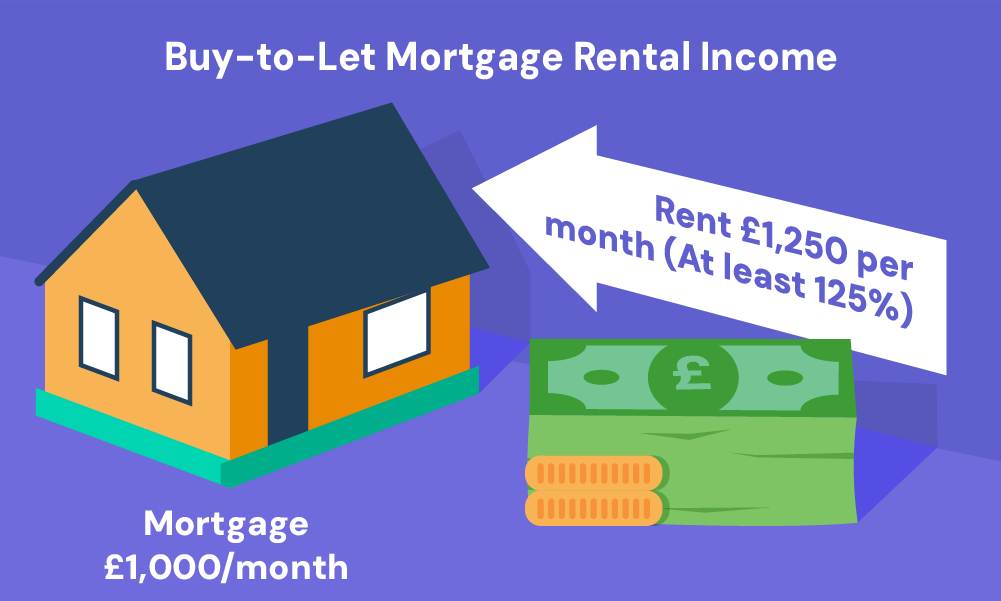

How Much Can You Borrow?

Lenders mainly assess your borrowing capacity based on the rental income you anticipate from the property.

This income is seen as your ability to cover the mortgage payments, along with any other costs. In general, they will want your rental income to cover between 125% to 145% of the mortgage payments.

Some lenders might assess the property’s rental value themselves, while others may use Association of Residential Lettings Agents (ARLA)* qualified letting agents.

Your personal income isn’t usually the main factor, but having a stable income can still positively influence your mortgage application.

Therefore, focusing on the property’s potential rental income is key when you’re self-employed and exploring buy-to-let mortgage options.

*ARLA is a UK professional body that sets standards and offers accreditation for letting agents, ensuring ethical practices within the industry.

Which Lenders Offer Buy to Let Mortgages for Self-Employed?

Finding the right lender for a buy-to-let (BTL) mortgage can be a unique challenge, especially if you’re self-employed. But, you’ll be pleased to know that various options are tailored to your situation.

The choice of lenders often depends on the specific property and your circumstances as a self-employed person.

Some lenders known for catering to self-employed applicants for BTL mortgages include:

- HSBC

- Santander

- Natwest

But this list is just the tip of the iceberg. To truly uncover the full spectrum of buy-to-let mortgages that suit your needs, it’s a wise idea to consult a knowledgeable advisor.

By engaging an expert broker who’s well-connected with lenders nationwide, you can ensure that you’ll be shown the very best options tailored to your situation as a self-employed individual.

Their insights and experience can guide you to the right mortgage without the guesswork.

Remortgaging a Buy-to-Let Mortgage

Remortgaging a buy-to-let property as a self-employed individual can be complicated, but it is possible with the right approach. The key is to understand the unique considerations that apply to your situation.

If you were self-employed when you first took out your mortgage and your financial situation has not changed much since the remortgaging process should be relatively straightforward.

However, if your employment situation has changed, especially if you were in full-time employment and are now self-employed, lenders may conduct thorough affordability checks.

What should you do? Buy-to-let mortgages often have introductory rate periods where your monthly payments are more affordable.

It’s wise to start shopping around for a remortgage at least six months before this period ends.

Key Takeaways

- Self-employed individuals can get buy-to-let mortgages, with many lenders specializing in or accommodating their needs.

- Lenders consider factors beyond income when assessing self-employed buy-to-let applications, such as landlord experience, credit history, property type, and location.

- Deposits for self-employed buy-to-let mortgages typically start at 25% of the property value, but some lenders may accept less.

- Lenders assess borrowing capacity for self-employed buy-to-let mortgages based on anticipated rental income, typically covering between 125% to 145% of mortgage payments.

The Bottom Line: Your Next Steps

Finding the right buy-to-let mortgage as a self-employed individual doesn’t have to be a struggle.

Mortgage specialists have access to lenders and products that might be out of your reach. They can sift through these to find the ones that suit your situation perfectly.

They understand the buy-to-let market and the unique challenges you face, guiding you to make decisions that align with your goals.

Rather than spending hours on research, let a specialist do the legwork for you. It simplifies the process and saves you time.

What makes specialists stand out is their effort to comprehend your unique needs. They present options tailored to you, not just generic products off the shelf.

Interested in getting matched with the right mortgage? Fill out this quick form, and we’ll connect you with a broker who’s ready to help you succeed in your property investment journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a buy-to-let mortgage if I'm newly self-employed?

Yes, but it can be more challenging. Lenders will typically want to see at least two years of trading history and financial statements. Some might have more flexible options, so it’s worth shopping around or consulting a specialist.

How are self-employed applicants assessed differently?

Lenders might ask for more in-depth financial records, such as profit and loss accounts, to gauge your financial stability. It often requires a more detailed examination of your finances compared to salaried applicants.

What sort of documents do I need for a buy-to-let mortgage if I'm self-employed?

You’ll likely need to provide proof of rental income, business accounts for the last two to three years, a copy of your self-assessment tax return, and details of the property you’re looking to buy.

Can I remortgage my property to a buy-to-let mortgage as a self-employed individual?

Yes, it’s possible to remortgage your property to a buy-to-let mortgage if you’re self-employed. You will still need to meet the lender’s buy-to-let eligibility and affordability criteria. It’s often wise to consult a skilled advisor to guide you through the process.

Is it still possible to find self-cert buy-to-let mortgages?

It seems that official self-cert buy-to-let mortgages aren’t available anymore, but I found that there are lenders willing to be quite accommodating for us self-employed folks. Apparently, as long as I can show that the rental income from the property is a sensible investment, I might not have to produce all my income details or business accounts.

Can I switch my current mortgage to a buy-to-let one since I'm self-employed?

From what I’ve gathered, switching to a buy-to-let mortgage as a self-employed person is doable. The process seems to resemble remortgaging, but the lender will want to see if I meet their criteria for buy-to-let, taking into account things like eligibility and affordability. It sounds like having an expert advisor to help guide me through this change might be a good idea.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

How To Remortgage When Self-Employed In The UK?

Remortgaging when you’re self-employed doesn’t have to be a headache. Sure, mortgage lenders want to see solid proof of income, and that can be a bit more complex when you’re working for yourself. But there’s good news: With the right support, YOU can switch your mortgage without a hitch. In this article, we’re going to […]

Mortgages for Self-Employed with 2 Years of Accounts

If you’re self-employed in the UK, you’re in good company with 4.31 million others. But what if you’re fairly new to this and want to buy a home? Can you get a mortgage with only two years of accounts? Don’t worry, we’ve got you covered. This article is a complete guide that answers these questions. We’ll […]

Self-Employed Mortgages Calculator – Crunch the Numbers Now

Being self-employed gives you the freedom to be your boss, but you’ve likely noticed that figuring out a mortgage is not as straightforward. The amount you can borrow varies depending on your work situation. Whether you’re a sole trader, in a partnership, a contractor, or a company director, the borrowing rules can change. So, how […]