- How Does Equity Release Interest Work?

- Current Equity Release Interest Rates

- What is the Best Rate You Can Get on Equity Release?

- Factors Affecting Equity Release Interest Rates

- Equity Release Interest Rates: Fixed vs Variable

- What are APR and MER and How Do They Differ?

- How To Lower Your Equity Release Interest Rates?

- The Bottom Line: Take the First Step

How To Find The Best Equity Release Rates in 2025?

In 2025, you might find yourself thinking about unlocking the cash tied up in your property.

Maybe you’re after a comfortable retirement, planning that dream holiday, or even eyeing up a nice little nest egg for your loved ones.

But, with so many equity release products out there, you might be left scratching your head, thinking which offers the best equity release rates? Well, that’s where we come in!

This guide dives straight into the details of equity release interest rates, helping you better understand how they work and how to get your hands on the best ones for your unique situation.

How Does Equity Release Interest Work?

When it comes to equity release, understanding how interest is calculated and added to your loan is crucial.

Over time, this interest can significantly increase the overall amount you owe.

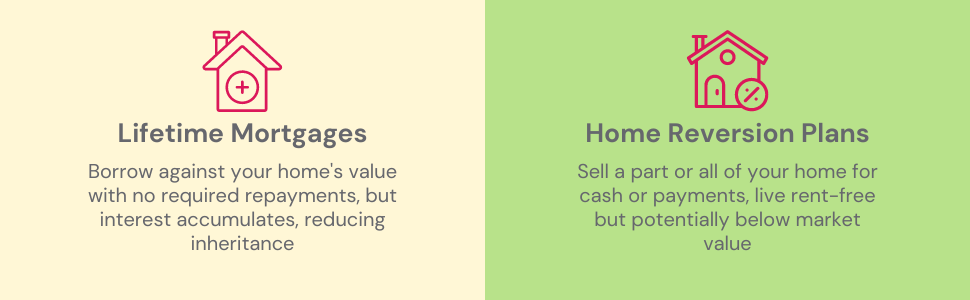

The two most common types of equity release products – Lifetime Mortgages and Home Reversion Plans – have different approaches to interest.

In a Lifetime Mortgage, you borrow a portion of your home’s value, and interest is charged on this amount.

Crucially, this interest is compounded, meaning that over time, you’re not just paying interest on the initial loan, but also on the accumulated interest. This can cause the loan balance to grow quickly.

For instance, if you take out a Lifetime Mortgage of £100,000 at an annual interest rate of 5%, after one year, you’d owe £105,000. The second year, you’d be charged interest on £105,000, making your debt £110,250, and so on.

On the other hand, a Home Reversion Plan involves selling a portion of your home for less than its market value, rather than borrowing against it. As such, it doesn’t accumulate interest in the same way.

It’s important to be aware of these potential implications, as equity release could impact the size of the estate you leave behind and your eligibility for means-tested benefits.

Always ensure you fully understand the terms and implications before proceeding with an equity release plan.

Current Equity Release Interest Rates

Equity release interest rates in the UK usually fall between 6% and 9%, but they don’t stay the same forever. They can go up or down, so the deals you see today might not be there next month.

The rate you get depends on things like how old you are, how much your house is worth, and what kind of plan you pick. Different companies also have their own rules and offers, which can change what’s available for you.

But interest rates aren’t the only thing you need to think about. There are extra costs, like fees for setting up the plan, checking the value of your house, and hiring a solicitor. These can all add up, so it’s smart to think about the total cost, not just the interest rate.

If you want the latest rates and advice, it’s a good idea to talk to a financial adviser or equity release expert. They can help you find a plan that suits you and make sure you understand all the costs involved.

What is the Best Rate You Can Get on Equity Release?

Several factors can affect the interest rate you’re offered for equity release.

To give you a hint, the best interest rate you might get on equity release in Aug 2023 is 5.74% (MER)*. Yet, this figure doesn’t paint the whole picture.

Why? As we said earlier, your own rate depends on your personal situation and the kind of equity release you choose. And keep in mind, rates can change.

Remember, while going for the lowest rate might seem like the best move,it doesn’t always mean you’re getting the best deal.

A lower rate could mean less to pay back over time, but it might also come with higher upfront costs or fewer flexible options. So, it’s important to look at the whole picture.

Consider the rate, any extra charges, and the plan’s rules and conditions to really understand what you’re getting.

*Just a quick note – rates may have changed since this article was last updated.

Factors Affecting Equity Release Interest Rates

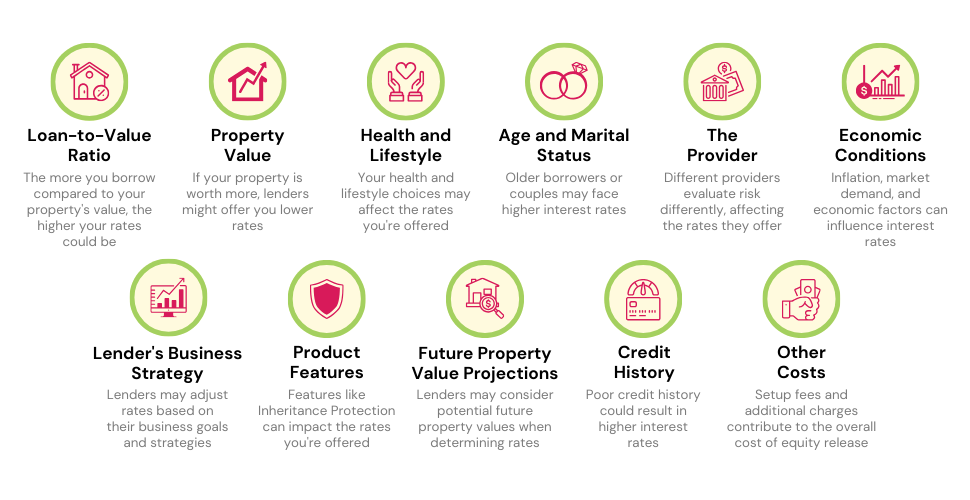

Equity release interest rates aren’t pulled out of the blue; they’re shaped by many factors:

- Loan-to-Value Ratio – This is a biggie. If you want to borrow a large chunk of your property’s value, you might find the interest rates creeping up.

- Property Value – Again, if your property is worth a lot, lenders might feel safer and offer you lower rates.

- Health and Lifestyle – Got certain health conditions or lifestyle habits? You might get what’s called an ‘enhanced’ plan with lower rates.

- Age and Marital Status – Older folks and couples applying together could find rates going higher. That’s because you can usually borrow more the older you are, which might bump up the rate.

- The Provider – Different providers have different rules and might assess risk differently. This could affect your rate.

- Economic Conditions – Things like inflation, the Bank of England’s base rate, and even demand and supply can push and pull the rates around.

- Lender’s Business Strategy – Sometimes, lenders might drop their rates to pull in more customers.

- Product Features – Certain features, like Inheritance Protection, might affect your rate.

- Future Property Value Projections – Lenders might consider what your home could be worth in the future.

- Credit History – A poor credit history doesn’t stop you from getting equity release, but it might stop you from getting the best deals.

- Other Costs – Don’t just look at the interest rate. Remember to check setup fees, early repayment charges, and the total cost.

So, while understanding these factors is handy, getting the best deal means looking at the big picture.

This often needs a professional’s touch, so it’s a good idea to get advice from a qualified broker or advisor.

Equity Release Interest Rates: Fixed vs Variable

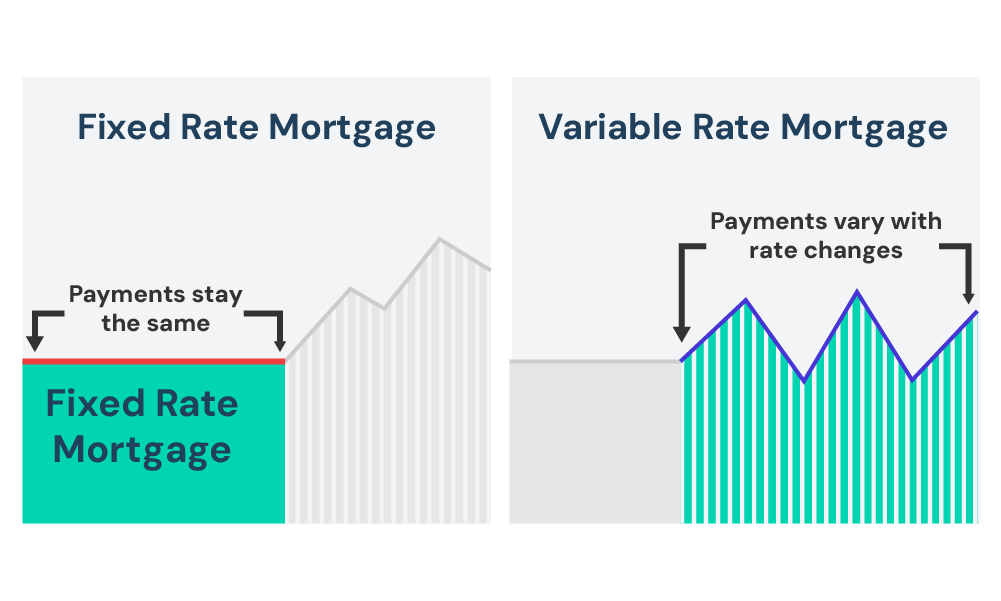

When considering equity release, it’s important to understand the two main types of interest rates you might encounter: fixed and variable rates.

Fixed rates remain constant throughout the loan’s duration, ensuring the amount of interest you pay doesn’t change over time. This is beneficial because it provides certainty about future loan costs, allowing for precise budgeting.

But, one potential drawback is that if general interest rates decrease, a fixed rate doesn’t change to reflect this, possibly resulting in higher interest charges than with a variable rate.

On the other hand, variable rates can alter over time, often linked to an external benchmark such as the Bank of England base rate.

The biggest perk is that you might save money if interest rates go down. But there’s a catch—if rates go up instead, you could end up paying more later on.

Pro-Tip

Remember, with equity release, you don’t usually pay off the interest during your lifetime. It usually gets settled when your property is sold, move into long-term care, or after you’ve passed on. Before choosing an equity release product, always weigh its advantages and downsides.

What are APR and MER and How Do They Differ?

APR stands for Annual Percentage Rate. It is a measure of the total cost of borrowing money, including interest, fees, and other charges.

The APR is expressed as a percentage of the amount borrowed, and it is calculated over a period of one year.

MER stands for Monthly Equivalent Rate. It is a measure of the cost of borrowing money, expressed as a monthly rate. The MER is calculated by dividing the APR by 12.

The main difference? APR includes any extra charges linked to the loan, while MER is all about the interest. This means that the APR is a more accurate measure of the true cost of borrowing money.

When comparing different loan options, it is important to look at the APR, not the MER. The APR will give you a more accurate picture of the true cost of borrowing money.

And remember, it can be really useful to chat with a financial advisor or use an online APR to MER calculator to understand these terms better.

What is an AER?

AER, which stands for ‘Annual Equivalent Rate‘. It’s typically used for savings accounts and shows the rate of interest you’d earn if it was paid and compounded each year.

How To Lower Your Equity Release Interest Rates?

Reducing the interest rate on your equity release can save you a significant amount in the long run. Here are some simple steps to take:

- Shop Around – Don’t settle for the first offer. Look for multiple options and compare their rates.

- Use a Broker – Professional brokers have access to exclusive deals and can assist you in finding the most suitable offer.

- Only Borrow What You Need – More substantial loans typically have higher interest rates. By only borrowing what you need, you can potentially secure a lower rate.

- Maintain Good Credit – While credit checks aren’t as stringent for equity release as regular mortgages, some lenders still consider your credit history.

But, it’s important to understand the potential risks associated with equity release. These could include reducing your estate’s value, impacting your eligibility for means-tested benefits, and possibly generating early repayment charges if you decide to repay the loan sooner.

The Bottom Line: Take the First Step

Understanding equity release interest rates is critical to informed financial decision-making. It’s not just about finding a low rate, but considering additional costs and the factors that influence them.

With equity release, remember, the interest builds up and is deducted from the sale of your property or when you move into care.

Getting professional advice is essential for a complete understanding. This is where specialist mortgage brokers shine.

They’re the best way to secure best rates, as they can sift through the complex market and guide you to an equity release plan that aligns with your financial aims and lifestyle.

Ready to get started? Fill out our quick form and we’ll connect you with a specialist mortgage broker who can offer expert guidance on your equity release journey. Don’t wait, get started today.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Are equity release interest rates higher than traditional mortgage rates?

Yes, equity release interest rates are usually higher than those of traditional mortgages. This is due to the added risk to the lender associated with equity release products.

Can I make interest payments on my equity release plan to reduce the amount owed?

Yes, making interest payments on your equity release plan can certainly help reduce the total amount owed.

How can my health impact the equity release interest rate I’m offered?

If you have certain health conditions, you might be eligible for an Enhanced Lifetime Mortgage, which can potentially offer lower interest rates or larger loans compared to standard equity release products.

How often are equity release interest rates reviewed?

The review frequency of equity release interest rates can vary by provider and product, often adjusted based on economic conditions.

How does equity release interest rates compare across different providers?

Interest rates do differ among providers, influenced by factors like the specific product offered and the Loan-to-Value ratio.

How do equity release interest rates vary by location within the UK?

Generally, equity release interest rates do not vary by location within the UK. The rates are more influenced by the specific product, your circumstances, and the amount you borrow.

Are variable interest rates available for equity release?

Yes, you can certainly get variable interest rates with equity release plans. But it’s worth noting that if the plan is sanctioned by the Equity Release Council, the rates must be capped to protect borrowers from steep interest hikes.

How long does it take to get a low-interest equity release plan?

The duration can vary. It largely depends on several factors such as your eligibility, property valuation, and the completion of legal paperwork. These processes can take anything from a few weeks to a few months. Being prepared with the necessary information and seeking legal and financial advice can speed up the process.

How does inflation affect equity release interest rates?

Inflation can lead to an increase in equity release interest rates. If inflation is high, the Bank of England may raise the base interest rate, which generally leads to increased rates for financial products, including equity releases.

This article has been fact checked

This article was created, checked, and verified by the expert team at Money Saving Guru. Trust us, you’re in good hands.

Related Articles

Can I Sell My House If I Have An Equity Release?

Selling your home with an existing equity release plan requires careful planning. Many homeowners considering a move – be it closer to family, downsizing, or a lifestyle change – often wonder if equity release complicates the sale. The good news is you can absolutely sell! 🎉 However, for a smooth process aligned with your financial […]

Equity Release Companies to Avoid in 2025: 8 Warning Signs

Equity release is a way for older people to get money from their home without having to sell it. It’s a big choice, so it’s normal to feel a bit unsure about which company to trust. Some companies are great, but others might not have the best intentions. So how do you figure out who’s […]

Equity Release Calculator – No Personal Details Required

Lifetime Mortgages are rapidly gaining traction across the UK, becoming a popular option for homeowners in their retirement years. If you’re curious about unlocking the equity in your home, you’ve come to the right place. How Much Equity Can You Release? Our equity release calculator will provide you with an immediate understanding of the equity […]