- What is a £2 Million Mortgage?

- Who Can Get a £2 Million Mortgage in the UK?

- What Deposit Do You Need for a £2 Million Mortgage?

- Steps to Secure a £2 Million Mortgage

- How Much Does a £2 Million Mortgage Cost Each Month?

- Additional Costs in £2 Million Mortgage Process

- Income Requirements for a £2 Million Mortgage

- How Does Your Income Type Impact Your Mortgage Application?

- The Bottom Line

How To Get a £2 Million Mortgage in the UK?

House prices in the UK, especially in places like London, have gone through the roof. This has made £2 million mortgages more common than you might expect.

Not long ago, mortgages like this felt out of reach for most people. Now, they’re becoming a realistic choice for buyers looking at high-end homes.

It’s a big step. But it doesn’t have to be confusing.

As demand for luxury properties grows, understanding how a £2 million mortgage works is key. Whether you’re just starting or ready to make your move, knowing the basics will help.

This guide keeps it simple. It’s here to help you take that next step with confidence.

What is a £2 Million Mortgage?

A £2 million mortgage is exactly what it sounds like—a loan of £2 million to buy a property.

With house prices climbing, especially in popular cities, these large mortgages are becoming more common.

They’re often needed for buying homes in upscale areas where prices have skyrocketed.

It’s a way to make up the difference between what you can afford and the cost of your dream home.

In today’s market, higher-value mortgages like this aren’t unusual. They’re simply part of keeping up with the rising cost of property.

Who Can Get a £2 Million Mortgage in the UK?

Getting a £2 million mortgage isn’t for everyone—it’s usually for people with high incomes, a strong credit score, and a big deposit (around 15-25% of the property’s value).

Here’s what lenders look at:

- Income: Lenders want to see that you earn enough to handle the repayments comfortably, along with any other financial commitments you have. A stable and sufficient income is key.

- Credit History: Your credit history shows how well you’ve managed debt in the past. A strong credit score not only improves your chances of approval but might also get you better mortgage terms.

- Debt-to-Income Ratio (DTI): This is the portion of your income that goes toward paying off debts. A lower DTI ratio is better, as it shows you have enough money left to cover a new mortgage. Not sure how yours stacks up? Use our DTI ratio calculator to check—it’s quick and easy!

- Employment History: Lenders prefer borrowers with steady jobs and consistent income. A reliable employment history is always a big plus.

- Assets and Savings: Your savings and assets show lenders that you can afford the deposit and extra costs, like stamp duty or legal fees.

- Property Type and Value: Lenders also consider the property you’re buying to ensure its value matches the mortgage amount you’re requesting.

If you tick these boxes, you’re on the right track. A good mortgage adviser can help you understand specific lender requirements and guide you through the process to increase your chances of approval.

What Deposit Do You Need for a £2 Million Mortgage?

For a £2 million mortgage, the required deposit typically ranges from 10% to 25% of the property’s value.

This means you may need to provide between £200,000 and £500,000 upfront.

The size of your deposit affects your mortgage terms: a larger deposit usually results in lower interest rates and better repayment conditions, as it decreases the lender’s risk.

Steps to Secure a £2 Million Mortgage

A £2 million mortgage might sound complicated, but it’s not too different from getting any other mortgage.

You just need to be a bit more prepared because of the larger amount.

Here’s how you can do it:

- Check Your Money. Take a good look at your income, savings, and any debts you already have. Make sure you’ve got important paperwork ready, like payslips and bank statements. Lenders will want to see these to check if you can afford the loan.

- Improve Your Credit Score. Your credit score shows lenders how good you are at managing money. Check your credit report, clear any unpaid debts, and fix any mistakes you spot. A good score can help you get better deals on your mortgage.

- Plan for Extra Costs. Buying a house isn’t just about the mortgage. You’ll also need money for things like stamp duty, legal fees, and surveys. These can add up, so make sure you’ve saved enough to cover them.

- Choose the Right Lender. Think about whether you want to go with a traditional bank or a private lender. Different lenders offer different options, so pick one that works best for your situation.

- Apply for the Mortgage. Once you’re ready, send in your application. The lender will check how much the property is worth and take a close look at your finances. If everything looks good, they’ll offer you the mortgage.

A mortgage this big can feel a bit overwhelming, but you don’t have to do it alone.

A good mortgage broker can guide you through the process, help you find the best deals, and make things much easier.

If you’d like some support, we can set you up with a free chat with a mortgage broker. They’ll help you figure out your next steps and get you closer to owning your dream home.

How Much Does a £2 Million Mortgage Cost Each Month?

Your monthly repayments for a £2 million mortgage depend on a few key factors:

- Interest Rate. This is what your lender charges for borrowing. Lower rates mean smaller monthly payments, while higher rates make them more expensive.

- Mortgage Term. This is how long you’ll take to pay back the loan. A longer term spreads out the cost, making monthly payments smaller, but you’ll pay more interest overall.

- Type of Mortgage. With a repayment mortgage, you pay off both the loan and the interest each month, so you’ll owe less over time. An interest-only mortgage lets you pay just the interest, keeping monthly payments low, but the full loan stays unpaid.

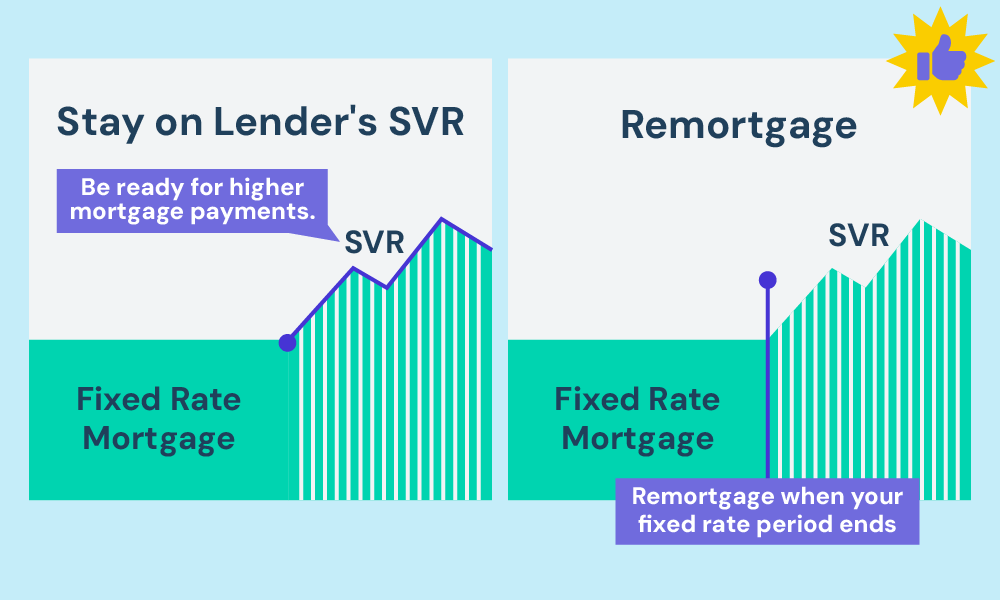

Fixed interest rates are popular in the UK because they keep your payments consistent for a set time—usually 2, 3, or 5 years.

After that, most lenders move you to their standard variable rate (SVR), which can be higher. At this point, you can either stick with the SVR or remortgage for a better deal.

Before we jump into the numbers, here’s a quick reminder: the table below is just an example. And it may not reflect the current mortgage market.

Your actual repayments will depend on your lender’s terms, the type of mortgage you choose, and the interest rate you’re offered.

Example Monthly Payments for a £2 Million Mortgage (2.5% Fixed for 5 Years)

| Mortgage Type | Monthly Payment (£) | Total Paid Over 5 Years (£) |

|---|---|---|

| Repayment Mortgage | £35,495 | £2,129,683 |

| Interest-Only Mortgage | £4,167 | £250,000 |

Fixed-rate mortgages are great for keeping your payments steady, but it’s worth planning for what happens after the fixed period.

If rates go up, your repayments could increase, so it’s good to have a plan in place.

If you need help working out your options, a mortgage adviser can guide you through the process and find the best deal for your situation.

To estimate how much you’ll pay for a mortgage, use our mortgage calculator.

Additional Costs in £2 Million Mortgage Process

When securing a £2 million mortgage, you’ll encounter several additional costs beyond the loan itself. Understanding and budgeting for these is crucial:

- Stamp Duty. This is a significant tax you pay when buying a property over a certain value. The amount varies based on the property price and whether it’s your first home or an additional property.

- Valuation Fees. Lenders require a property valuation to confirm its worth matches the loan amount. This fee depends on the property’s value and the lender’s requirements.

- Legal Fees. Hiring a solicitor or conveyancer is necessary for the legal aspects of buying a property. Their fees can vary widely.

- Arrangement Fees. Some lenders charge a fee for setting up the mortgage. These can be substantial, especially for high-value loans.

- Broker Fees. If you use a mortgage broker, they may charge a fee for their services.

- Survey Costs. Getting a detailed survey of the property can identify any potential issues. Costs vary based on the survey type and property size.

To manage these costs, start by getting detailed quotes for each expense. This helps you create a comprehensive budget.

Setting aside a contingency fund for unexpected expenses is also a wise move.

Income Requirements for a £2 Million Mortgage

For a £2 million mortgage, lenders typically look for a high and stable income. This assures them that you can comfortably manage the hefty monthly repayments.

Here’s how income affects your borrowing capacity:

- Lender’s Income Multiplier. Lenders often use an income multiplier to decide how much they’ll lend you. For example, if a lender uses a 4x multiplier and your annual income is £500,000, you could potentially borrow up to £1.2 million.

- High-Income Exceptions. Some lenders might offer higher multipliers for high earners, potentially lending up to 5x or 6x your income in certain circumstances.

- Income Stability. Lenders also consider the stability and source of your income. A steady job, consistent earnings, or reliable self-employment income are looked upon favourably.

- Other Income Sources. Income from investments, bonuses, and other sources can also be considered, improving your borrowing power.

Remember, each lender has different criteria, so it’s important to shop around or consult with a mortgage broker to find the best option for your financial situation.

How Does Your Income Type Impact Your Mortgage Application?

Your income plays a big part in how lenders decide if you can afford a mortgage.

If you have a regular salary from an employer, things are usually pretty simple. Lenders can easily check your payslips and assess how much you can borrow.

But if your income comes from self-employment, freelance work,, dividends, or investments, things can get a bit trickier.

Lenders need to make sure your income is stable and reliable, especially if it changes from month to month or comes from different sources.

In these cases, they might look at your average income over a few years or focus on the most stable parts of what you earn. It’s important to show your income clearly so lenders can see it’s consistent and trustworthy.

If your income is more complex, a mortgage broker can be a huge help. They know which lenders are more flexible with non-traditional income and can guide you through the process to make everything as smooth as possible.

The Bottom Line

With house prices on the rise in many parts of the UK, especially in popular areas, more and more people are looking at bigger mortgages.

A £2 million mortgage is becoming a common choice for those wanting a top-notch home.

This is partly due to rising costs and the appeal of luxury properties, so it’s important to know what’s involved in getting such a big mortgage.

First off, think about what you can afford.

For a mortgage this size, you usually need a deposit between £200,000 and £500,000, which affects your mortgage’s terms and how much interest you’ll pay. Your income is really important too.

Lenders will check how much you earn and your past money (your credit history) to make sure you can handle the repayments. And remember, there are extra costs like stamp duty and legal fees when buying a house.

It can feel pretty daunting to sort all this out by yourself.

This is where chatting with a mortgage advisor can make a big difference. They’ll give you advice that suits your situation, helping you get your head around different mortgage options and what each step involves.

Thinking about a big mortgage? We can give you a hand. Get in touch with us, and we’ll put you in contact with a specialist mortgage advisor to help you get started with your journey.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I get a £2 Million commercial mortgage?

Yes, you can obtain a £2 million commercial mortgage. These are available for purchasing business properties or refinancing existing commercial property.

The criteria for eligibility include a strong business financial history, proof of stable income from the business, and often a solid business plan.

Lenders will also assess the value and condition of the property being mortgaged. The terms and interest rates can vary depending on the lender and your business credentials.

What are the challenges with high-street banks for high-value mortgages?

High-street banks often have more stringent lending criteria for high-value mortgages, which can pose challenges for borrowers.

They may have lower maximum loan-to-value ratios, require a more extensive credit history, and be less flexible with income types.

Additionally, high-street banks may not offer the bespoke services that high-net-worth individuals require.

As alternatives, private banks and specialist lenders often provide more tailored services, with a willingness to consider complex income sources and offer more flexible terms.

What do specialist lenders offer for £2 million mortgages?

Specialist lenders provide bespoke services for £2 million mortgages, catering specifically to high-net-worth individuals and those requiring large loans.

These services include more flexible criteria for income assessment, consideration of non-traditional income sources, and potentially higher loan-to-value ratios.

Specialist lenders often provide personalised attention, understanding the unique financial situations and needs of each borrower.

Their approach is more tailored compared to standard mortgage products offered by traditional banks, allowing for more customised loan solutions.

Related Articles

Private Mortgage Lenders Explained

You didn’t get where you are by settling for ordinary, so why start now? Regular mortgages might work for most people, but when you’re dealing with serious wealth, they just don’t measure up. Private mortgages, on the other hand, are in a league of their own. Whether it’s a stunning countryside estate, a sleek London […]

Securing High Net Worth Mortgage In The UK

If you’re wealthy, regular mortgages probably don’t work for you. You need something designed to match your lifestyle and financial goals. The good news? With the right mortgage advisor, buying a high-value property or using your assets for smart investments can be simple. This guide breaks down high-net-worth mortgages in 2025, so you can see […]

The Complete Guide To Asset Based Mortgages In the UK

Lenders often seem to miss the bigger picture when it comes to wealth. You could have millions in property, shares, or investments, but if your income doesn’t tick their boxes, they might still turn you down for a mortgage. That’s where asset-based mortgages come in. Instead of focusing on your income, these mortgages consider the […]