- What Qualifies as a Second Home?

- Mortgages for Second Homes: What You Need to Know

- Buy-to-Let Mortgages: Investing in Rental Properties

- How Stamp Duty Works for Second Homes

- Check Your Second Home Stamp Duty With Our Calculator

- Buying a Second Home for Your Children

- Pros and Cons of Buying a Second Home in the UK

- The Bottom Line

What Is Classed As A Second Home In The UK?

Thinking about buying a second property? Maybe a cosy cottage in the countryside for weekend escapes, a chic city flat for rental income, or even a seaside retreat for family holidays.

Whatever your plan, you need to know how the UK classifies second homes.

This isn’t just about ticking boxes – different tax rules, mortgage requirements, and ownership laws come into play.

So, let’s dive into what makes a second home in the eyes of the government.

What Qualifies as a Second Home?

Any property you own, aside from the one you consider your primary residence, is generally regarded as a second home. This could include a variety of scenarios, such as:

- A holiday home or vacation property

- A buy-to-let or rental property for investment purposes

- A home owned jointly with a family member

- A property purchased for your children’s use

The key factor is that it’s not your main place of residence, where you live most of the time and consider your permanent home.

Mortgages for Second Homes: What You Need to Know

If you’re considering purchasing a second home, it’s essential to understand the mortgage options available and the associated requirements.

Funding Options for Second Homes

There are several ways to fund the purchase of a second home for your own private use:

- Cash Purchase. If you have sufficient funds available, you can opt to buy the property outright without needing a mortgage.

- Remortgaging. If you have little or no outstanding mortgage on your main residence, remortgaging could be a viable option. This would allow you to release equity from your primary home to fund the purchase of a second property. However, be mindful of any potential costs associated with breaking your existing mortgage terms.

- Equity Release. If you’re over 55, you could explore equity release schemes like a lifetime mortgage. This option enables you to release a lump sum from the equity in your main residence without making monthly payments. The interest accrued is rolled up until the property is sold when you pass away or move into long-term care.

- Second Home Mortgages. Many lenders offer specialised second home mortgages for those with an existing property who wish to purchase another one.

Requirements for Second Home Mortgages

Getting a second home mortgage typically involves tougher hurdles than a regular mortgage. Here’s what you’ll need to be prepared for:

- Bigger Deposit. Lenders will ask for a larger deposit, usually between 15% and 25% of the property value.

- Stricter Affordability Checks. They’ll rigorously assess your ability to afford the repayments, especially if you already have a mortgage on your main home.

- Higher Interest Rates. Expect to pay a higher interest rate on your second home mortgage compared to your primary residence.

- Proof of Income. You’ll need to provide detailed evidence of your income, including tax returns, payslips and bank statements, to prove you can handle the extra mortgage payments.

- Good Credit Score. A higher credit score is often required for a second home mortgage.

- Insurance. Be ready to show proof of insurance for the second property, including homeowners insurance and possibly additional coverage.

- Property Usage. Lenders will want to know if you plan to use the second property for personal use or as a rental investment.

- Debt-to-Income Ratio. They’ll closely examine your debt-to-income ratio to ensure your finances are stable. Generally, a lower DTI ratio is appealing to most lenders. Check if your DTI ratio qualifies for a mortgage here.

- Occupancy Requirements. Some lenders may have rules about how often you must occupy the second home each year.

- Reserve Requirements. Lenders might require you to have savings or reserves that can cover several months’ worth of mortgage payments for both properties.

These stricter requirements are in place to make sure you can comfortably manage the extra financial burden of owning a second property.

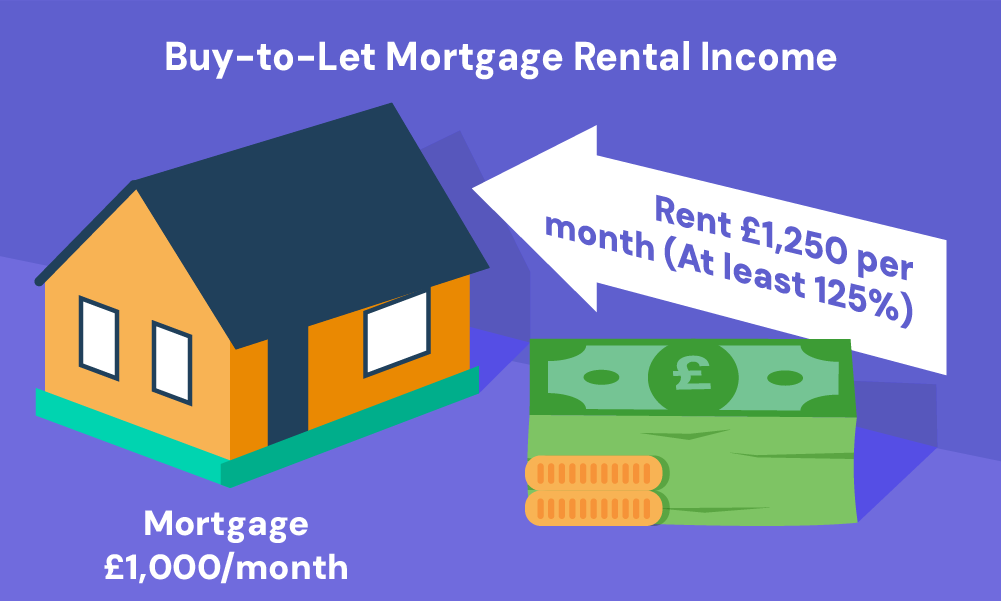

Buy-to-Let Mortgages: Investing in Rental Properties

Most lenders will recommend a buy-to-let (BTL) mortgage as the best option for this.

While the deposit you need for a BTL mortgage is similar to a second home mortgage (around 15% to 25%), how they assess affordability is different.

Instead of looking just at your income and expenses, lenders focus on the property’s potential as an investment.

They’ll want to see the expected rental income and will typically require it to cover at least 125% to 145% of the mortgage payments. This ensures the rental income can comfortably handle the mortgage costs.

How Stamp Duty Works for Second Homes

In the UK, buying a property or land triggers a tax called Stamp Duty Land Tax (SDLT). It’s a tiered system, meaning the more expensive the property, the more tax you pay.

For your main residence, there’s no tax on the first £250,000 of the value.

But for second homes, this benefit disappears – you pay a flat 5% surcharge on the entire purchase price.

Here’s an example: If you buy your first home for £200,000, you pay no stamp duty. But if you buy a second home for the same price, you’ll owe £6,000 (5% of £200,000) in stamp duty.

There are a couple of exceptions.

This surcharge doesn’t apply to very cheap second homes (under £40,000) or to moveable dwellings like caravans or houseboats.

Here’s an overview of SDLT rates in England and Northern Ireland (valid until 31 March 2025):

| Property Value Band | Standard Rate | Additional Property Surcharge | Total Rate for Additional Properties |

|---|---|---|---|

| Up to £250,000 | 0% | 5% | 5% |

| £250,001 to £925,000 | 5% | 5% | 10% |

| £925,001 to £1.5 million | 10% | 5% | 15% |

| Over £1.5 million | 12% | 5% | 17% |

Claiming a Refund for SDLT on Second Homes

If you’ve purchased a second home with the intention of making it your main residence, you’ll still need to pay the additional 5% surcharge initially.

But, if you sell your first property within 3 years, you can claim a refund from HMRC for the amount paid in the surcharge.

Check Your Second Home Stamp Duty With Our Calculator

Before you dive in, consider the Stamp Duty Land Tax (SDLT) you’ll need to pay. It can be a significant cost, so it’s wise to factor it into your budget.

This handy SDLT calculator can help you check the tax you owe.

Simply enter the property purchase price and click “Calculate”. The calculator will show you the SDLT amount based on current rates for second homes in the UK.

Buying a Second Home for Your Children

Helping your children get on the property ladder by buying them a house outright or becoming part-owners is a kind thing to do.

But be aware that this will be classed as a second home for tax purposes.

To avoid the extra stamp duty surcharge and stricter mortgage requirements, there are other options to consider:

- Help with their deposit.

- Be a guarantor on their mortgage, so you’ll help with repayments if they struggle financially during the mortgage term.

Talking to a qualified mortgage broker can help you find the best way to support your children without the downsides of buying a second home.

Pros and Cons of Buying a Second Home in the UK

Owning a second home in the UK can be tempting, but it’s a big decision. Here’s what to consider:

Pros:

- Investment. A second home could increase in value over time, giving you a nest egg for the future.

- Rental income. Renting it out when you’re not there can bring in steady cash to offset the costs and maybe even make a profit.

- Weekend escapes. No more expensive hotels! You’ll have your own place for getaways and holidays.

- Lifestyle perks. Fancy a change of scenery? A second home offers a relaxing escape and a chance to explore new places.

- Inheritance planning. It can be a valuable asset to pass down to future generations.

Cons:

- Financial burden. Second homes are expensive. You’ll need a big down payment, mortgage repayments, and ongoing maintenance costs. This can limit your ability to invest elsewhere.

- Extra expenses. On top of the mortgage, there are bills, council tax, insurance, and upkeep to consider. These can quickly add up.

- Higher stamp duty. You’ll pay a bigger chunk of Stamp Duty Land Tax compared to your main home.

- Rental challenges. Finding reliable tenants, dealing with empty periods, and managing repairs from afar can be tricky.

- Limited use. If you don’t use it often, it’ll sit empty, costing you money without any benefit.

The Bottom Line

Owning a second home in the UK can be a smart investment or a handy way to own a vacation home.

But before diving in, it’s important to understand the rules and costs involved. Mortgages, stamp duty – there’s extra legwork compared to buying your main home.

One way to simplify things is to use a whole-of-market mortgage broker. They have access to many mortgage options and can find the best fit for you.

Plus, they handle the tricky details, freeing you up to focus on the fun stuff – like planning afternoon teas on the patio of your new retreat.

Let them do the hard work so you can enjoy the benefits of your second home sooner. Why go it alone when an expert can take care of the heavy lifting?

Get in touch with us, and we’ll connect you with a qualified mortgage broker who can find the BEST deal for your second home purchase.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

Can I rent out my second home?

Yes, you can rent out your second home. However, you’ll need to obtain a buy-to-let mortgage specifically designed for rental properties.

These mortgages have different affordability criteria based on the expected rental income rather than your personal income.

Do I have to pay council tax on my second home?

Yes, you’ll need to pay council tax on your second home, even if it’s unoccupied for part of the year. However, some local authorities offer discounts for second homes that are unoccupied for extended periods.

Can I use my second home as a primary residence at some point?

Absolutely, you can use your second home as your primary residence in the future. If you plan to do so, make sure to inform your lender and local council, as this will affect your tax obligations and potentially your mortgage terms.

Can I claim tax relief on my second home?

If you’re renting out your second home, you may be able to claim certain tax reliefs on expenses related to the property, such as mortgage interest, maintenance costs, and letting agent fees.

Consult with a tax professional or accountant to understand your eligibility and requirements.

Do I need additional insurance for my second home?

Yes, it’s advisable to have separate insurance coverage for your second home, as it will have different risks and requirements compared to your primary residence. Many insurers offer specialised policies for second homes or holiday homes.

Related Articles

How To Get Consent To Let To Buy Another Property?

Renting out your current home to become a landlord is tempting, especially if you’re moving, your family needs more space, or you want to try property investment. But before you put up “For Rent” signs, check with your mortgage lender. You’ll likely need their permission to rent out your property. While it can be a […]

Calculate Your Second Home Mortgage in the UK

Thinking about buying a second home? Maybe it’s a cosy cottage by the coast or a city apartment for those weekends away. It’s an exciting idea, but it also makes you wonder—can you really afford it? Luckily, using a second home mortgage calculator can help you find out if this dream is possible. In this […]

Second Home Mortgage Rules and Requirements in the UK

Purchasing a second home can be an exciting milestone. Perhaps you want a holiday getaway, maybe you’re looking to invest in property, or you simply need more space for a growing family. Whatever your reasons, a second home mortgage opens doors to new possibilities. But, second home mortgages have unique rules and requirements you must […]