- What Are Large Bridging Loans?

- Why Large Bridging Loans Are a Big Deal

- How Much Can You Borrow?

- What Are the Main Uses for Large Bridging Loans?

- What Kinds of Properties Are on the Table?

- Who is Eligible for a Large Bridging Loan?

- What Paperwork Do You Need?

- Lenders and Rates: What To Expect?

- Can You Use a Large Loan for Auction Property?

- Is Bad Credit a Deal-Breaker for Large Bridging Loans?

- Are There Any Alternatives?

- The Bottom Line

Large Bridging Loans: Quick Cash for High-Value Properties

If you’re considering a big financial step and need quick access to a substantial amount of money. Large bridging loans might be your answer.

However, let’s be clear: This is big money we’re talking about. Taking out such a loan is a serious commitment.

In this guide, we’ll break down what large bridging loans are, how much they’ll cost you, and the things you need to consider before diving in.

What Are Large Bridging Loans?

In the UK, a large bridging loan starts at £2 million. These aren’t your regular loans; they give you the quick cash and flexibility you need, especially when you’re looking at property investments in England and Wales.

Types of Properties You Can Invest In:

- Homes

- Business properties

- Mixed-use buildings

- Newly built properties

The main point of these loans is to fill the financial gap when you’re buying high-value properties like a posh flat in central London or several lower-value homes. They let you move forward with new purchases while you’re waiting to sell other assets or sort out long-term financing.

Why Large Bridging Loans Are a Big Deal

Here’s the cool part: Large bridging loans let you make those big, complicated buys quickly. You don’t have to deal with all the red tape you’d find at a regular bank.

This speed means you can grab opportunities before they slip away. Plus, you get extra time to line up more traditional financing.

But that’s not all. If you’re looking at multiple units, like a whole block of flats, you can wrap it all up in one large bridging loan.

That way, you don’t have to juggle a bunch of smaller loans. It makes everything a lot simpler for everyone involved.

How Much Can You Borrow?

For large bridging loans, you’re generally looking at a range from £2 million up to £50 million. But it’s not set in stone. How much you can borrow depends on what you need and the value of the property you’re putting up as collateral.

Some lenders even start as low as £100k if that’s all you need. Typically, you can borrow up to 75% of your property’s value, known as 75% Loan to Value (LTV).

Don’t Rush Into It

Let’s get one thing straight: Bridging loans are usually a last resort.

Why? Because they’re expensive.

Besides needing to repay the full amount by a certain date—either fixed or flexible—you’re also looking at higher interest rates and additional fees. If you’re going after a really big loan, you might even need to put down a larger deposit.

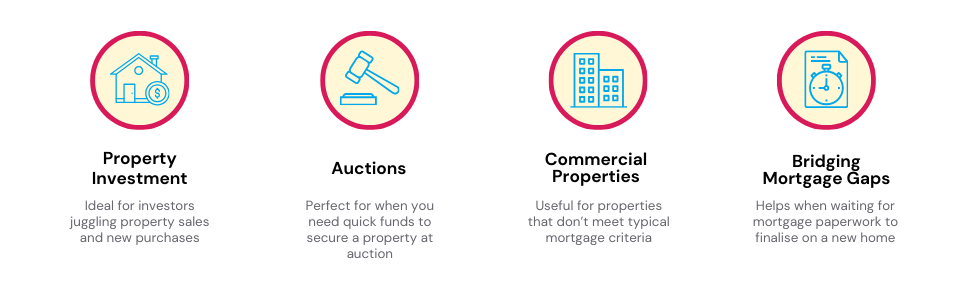

What Are the Main Uses for Large Bridging Loans?

Think of large bridging loans as your financial fast track. These loans are perfect when you need a large sum—starting at £2 million—really quickly.

Let’s say you’re an investor juggling a pending property sale while eyeing another tempting buy. Or maybe you’re bidding on a dream property at an auction, but your traditional mortgage hasn’t come through yet.

It’s also a lifesaver for those dealing with commercial properties or renovation projects that don’t yet meet typical mortgage criteria. Or perhaps you’re simply waiting for your mortgage paperwork to finalise and don’t want to miss out on locking down that perfect home.

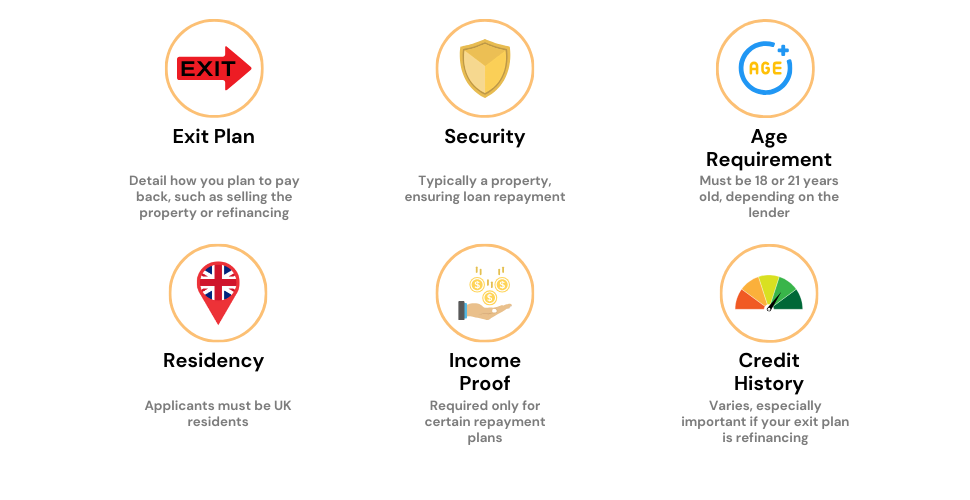

No matter the reason, one thing’s for sure: you’ll need a solid exit plan to show how you’ll pay back the loan.

What Kinds of Properties Are on the Table?

With a large bridging loan, you can buy all sorts of properties in England and Wales. You’re not just limited to luxury city flats; we’re talking about huge country houses that sprawl across acres of land.

You can also go for different types of property, like a residential place you want to rent out, big shopping centres, or even hotels. The choices are plenty, so it’s a good idea to chat with an expert to figure out what fits your needs.

Who is Eligible for a Large Bridging Loan?

If you’re interested in UK property and need quick funds, large bridging loans could be the answer. But remember, the property you want to use as security should be valued at at least £2.7 million.

So, who can get in on this?

- High-net-worth individuals

- Property investors

- Business owners with limited companies

- Foreign investors, whether they’re individuals or companies

- UK expats

Special Treatment for High Earners

If you pull in a net income of at least £300,000 annually or own assets worth roughly £3 million, you could enjoy some added flexibility.

The Financial Conduct Authority may offer you certain exemptions, allowing lenders to consider a wider range of factors when reviewing your application. This opens up more doors for you in terms of loan opportunities.

What Lenders Look At

When it’s about large bridging loans, traditional markers like credit score and regular income aren’t the be-all and end-all.

However, lenders aren’t just going to hand out large sums without being certain you can handle it. What they’re really looking for is your ability to repay the loan and a rock-solid exit strategy.

🌟 Pro Tip: Your Exit Strategy Matters 🌟

Before you secure a large bridging loan, make sure to outline how you’ll pay it back. Lenders need to see a clear plan, so here are some commonly accepted exit strategies:

- Switch to a long-term mortgage after the loan period.

- Sell the property to cover the loan amount.

- Offload other assets in your portfolio.

- Use an upcoming cash settlement, like an inheritance.

- Property developers can opt for development exit finance.

- Landlords might use specialised buy-to-let mortgages.

Having a solid exit strategy not only beefs up your application, but it also puts lenders at ease.

Additional Factors to Consider

- Deposit. Even if you’re rolling in it, you’ll need a sizable deposit—somewhere between 30% and 35%. If the loan is high-risk or super large, you might need to cough up 40%.

- Credit Score. Your financial past won’t haunt you too much unless it jeopardises your exit strategy. But a good financial history is always a plus.

- Experience in Property. If your loan is geared towards property development or investment, your track record in the field can significantly influence a lender’s decision. Newcomers might still find opportunities, but seasoned professionals will have the upper hand.

What Paperwork Do You Need?

To get your large bridging loan processed, you’ll need a few essential documents. Here’s what most lenders ask for:

- The reason you need the loan and how you’ll use it.

- Your exit strategy details (See our Pro Tip above on exit strategies).

- Whether the property is owned by an individual or a company.

- Information about the property you’re using as security, including its full address, value, and any remaining mortgage balances.

- Rental income details if the property is rented out.

- A statement outlining your assets and liabilities.

Additional documents may be required, but the lender will give you more details tailored to your situation.

Lenders and Rates: What To Expect?

The market for these loans is buzzing with specialised lenders like Holme Finance Bridging Solutions and Mint Property Finance.

Rates can differ a lot. You might see rates as low as 0.49% or as high as 2% per month.

High-net-worth folks have a leg up here; you can often get better rates by using valuable assets like yachts or gold as collateral. Traditional banks can’t offer these specialised loans, but a savvy broker can connect you with the right lender.

Can You Use a Large Loan for Auction Property?

Yes, you can. While large bridging loans can go up to £50 million, auction finance usually maxes out at £20 million.

This means you have plenty of scope to invest in high-end real estate, whether it’s luxury apartments, blocks of flats, or commercial units.

And here’s the kicker: auction finance funds can be in your account within 28 days, helping you meet tight auction deadlines.

Is Bad Credit a Deal-Breaker for Large Bridging Loans?

Absolutely not. Specialist loans are available even for those with a less-than-stellar financial history, including missed payments, CCJs, or bankruptcies.

Lenders assess each application individually, taking into account broader market conditions. They’ll let you know upfront how your credit history will affect your loan and repayment terms, so you’ll know exactly where you stand.

Are There Any Alternatives?

Bridging loans can be expensive. If you’re a high-net-worth individual, you might have other options like Lombard loans, which are backed by assets such as insurance policies or stock portfolios.

However, these financial instruments can be complex, so it might be wise to consult with a financial expert.

If you’re not in a rush, you might consider these less costly options:

- Development Finance – This could be a viable path if you’re looking to finance a development project.

- Second Mortgage – If it fits your situation and you meet the eligibility criteria, a second mortgage could be your answer.

- Secured Loan – Traditional lenders might offer options if you already own property and meet the eligibility criteria for a secured loan.

- Equity Release – Consider remortgaging your current property to finance a new one.

The Bottom Line

When it comes to large bridging loans, the market can be a tough place to make sense of. These types of loans aren’t overseen by the Financial Conduct Authority, which can make things even more complicated.

A skilled bridging finance broker is invaluable in such a setting. They can offer you expert advice, negotiate the best deals, and save you money in the process.

Traditional banks generally aren’t players in this specialised market, but brokers have connections to niche lenders who are. By leveraging a broker’s experience and network, you could end up saving a substantial amount of money.

So, don’t try to tackle this on your own. For a free, no-obligation chat, reach out to us. We’ll put you in touch with a broker who specialises in large bridging loans to help you make well-informed choices.

Get Matched With Your Dream Mortgage Advisor...

Find out if you qualify today by taking the M-Quotient™ Assessment for FREE!

Find my dream advisor & mortgage

(Won’t impact credit score)

Frequently asked questions

Find answers to common questions here.

What sets large bridging loans apart from regular bridging loans?

The primary difference between large and regular bridging loans is the size of the loan itself. Aside from that, the process for approval, the documents needed, and the speed at which the loan can be secured are essentially the same. Borrowers also have the flexibility to choose interest payment options that best fit their needs.

Do larger bridging loans come with higher interest rates?

Interest rates for bridging loans can vary based on several factors, such as your down payment, economic conditions, and fluctuations in the base rate. Importantly, the size of the loan itself generally does not lead to higher interest rates.

How big a bridging loan can I get?

The size of the bridging loan you can obtain depends on various factors like the value of the property or asset you’re using as collateral, your credit history, and your repayment plan. Loan sizes can range from smaller sums to amounts up to £50 million or more, depending on the lender’s terms and your financial situation.

Can you get a 100% bridging loan?

Yes, you can. However, getting a 100% bridging loan is extremely rare and generally not offered by most lenders. Lenders usually require some form of down payment or additional collateral as a safety measure.

If you’re looking for high loan-to-value ratios, some lenders may go up to 75% or 80% of the property’s value, but this will depend on various factors like the strength of your exit strategy and the quality of the asset used as collateral.

Related Articles

An In-Depth Guide To Secured and Unsecured Bridging Loans

If you’re in the UK and planning a big move—maybe you’ve found your dream home or you’re eyeing a property investment—you’ve got some financial decisions to make. One of them is choosing between a secured and an unsecured loan. Why does this choice matter? The loan you choose impacts your interest rate, borrowing limit, required […]

Second and Third Charge Bridging Finance Explained

When cash flow gets tight and traditional loans aren’t cutting it, you don’t have to hit the panic button. Second or third charge bridging loans can be your financial lifeline. Now, you might be thinking, “That sounds great, but what’s the catch?” Well, there are a few nuances you should be aware of, like varying […]

Fast Bridging Loans: How to Apply and What You Need?

Imagine you’ve spotted the perfect property investment—fantastic location, huge potential, and it’s a steal. There’s just one hitch: your assets are tied up, and the clock is TICKING. You’ve been down this road before—missing out because the cash wasn’t there when you needed it. But what if there was a way to make your assets […]